Updated 9-1-22

José Augusto Araújo, CEO/President of Brazilian dealership group Maqcampo, shares additional context to Farm Equipment’s questions on the Brazilian farm equipment industry.

Maqcampo is a John Deere group in Brazil that employs 700 across 19 stores and service points in four Brazilian states. The group, which is building 5 new facilities, maintains $20 million in parts inventory and spent $2 million in training last year (22,000 hours)

How does the labor shortage at dealerships and/farmers compare to the U.S.?

I think the shortage of labor is a global problem. There is a huge shortage of manpower, especially the technicians, which requires professional apprehension. We'd better talk about what we're doing to reverse this. Today we have a program, called Maqtrainee, that captures young people who have only finished high school and prepares them for the job market. Our goal is to train our entire team, and to specialize them through continuing education programs.

In what areas are U.S. farming and its equipment dealers more advanced than those in Brazil?

American resellers have some advantages over Brazilians. First, the quality of people's basic education. Young Americans have a better educational base, which makes learning easier.

Second is the capillarity of stores. Much closer to the farmer, this generates a better availability of equipment, still corroborated by a higher labor productivity.

Third, with a younger and more mature machine fleet and the advantage of having a resale market, U.S. industry can take advantage of several sales turns on the same asset, among others.

In what areas is Brazil farming and its equipment dealers more advanced than the U.S.?

As incredible as it may seem, it is the adoption of technology. The average age of Brazilian farmers is approximately 40 years, and therefore much more adept at technology. Thus, distributors have specialized in offering the technologies and transmitting the knowledge to use them. With the challenge of serving the Brazilian customer who is located over huge distances, the centralization of service, which compiles information to provide faster service and remote solution, and decentralizing only the physical interventions that are necessary, has been a differential for Brazilian resellers.

On August 4, I participated in a presentation alongside 4 equipment dealers to a group of dealers and farmers from Brazil that was on a weeklong benchmarking tour in the Midwest. The dealer participants included Bob Sinclair, Sinclair Tractor (John Deere); Stacy Anthony, AgRevolution (AGCO); Jason Searles, Coleman Tractor (Kubota); and Frank Lulich, Titan Machinery (Case IH)

Following a discussion on a variety of business and technology topics, I got a few minutes with the Brazilians group and inquired of the greatest differences they’d seen vs. their U.S. dealer brethren. Speaking through a translator, the officials replied that the technologies and products are generally the same as new products are launched simultaneously in both regions.

While they were shocked by the dearth of technicians and labor (“we never thought we would hear that coming here”), the greatest difference between the two dealer markets, they said, is in the structure and culture of the respective customer base.

Customer Base Differences

They noted the higher age of the U.S. farmers and how most farms are family enterprises where the owners often operate the machinery themselves. Farms are much smaller in the U.S. than those in Brazil. In their semi-arid of Brazil, where 90% of the ag money exists, large corporations own the land.

“What customers value is the same across the world. How the product performs, how well the dealer maintains the parts/service uptime, and how much that all costs the farmer…”

These farm operations have separate departments for procurement, engineering, IT and HR, just like any corporation. As a result, many dealer employees are involved with many different touchpoints into the farm customers. Brazilian dealers must attract and connect with the experience of many departments, so the purchasing journey is a longer one than in the U.S.

Brazilian dealers require more specialized personnel to deal with the specialized personnel on the other side of the fence. They described it as two big companies doing business, rather than two small family business interacting. The dealers also added that the back-office teams at their dealerships in Brazil are more robust than what is commonly seen in the U.S. model.

Brazilians like technology that makes it easier for the human relationship to take place, but the face-to-face is still very important.

Brand & Pricing

Another significant difference is pricing strategy. They say the pricing strategy is very different according to how the OEMs choose to produce the parts and equipment, whether they import parts or how they’re going to build and when, and which products will be made available in each region.

Large, Protected Territories for Major Ag Producing Country

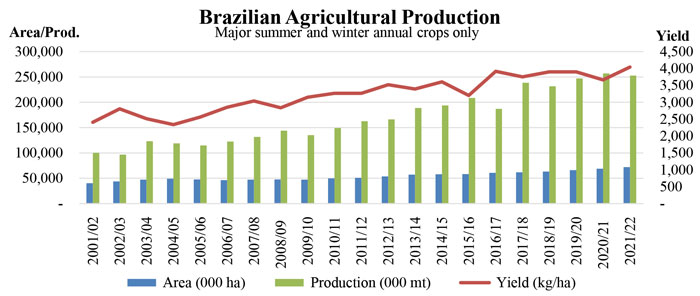

As a major agricultural producer (tops in the world for soybeans, second for beef/chicken and third for corn and pork), Brazil’s entire ag economy is served by a mere 800 equipment dealerships, with John Deere topping the list with 280 stores, owned by 38 groups. When told of the total numbers of U.S. farm equipment dealers (5,000 rooftops), the group answered that territories are protected by law.

Brazil’s agricultural GDP growth is estimated by USDA and others at near 4% annually, though more modest for 2022 due to the volatility that could accompany the October elections.

Source: MAPA/CONAB (Ministry of Agriculture, Livestock and Supply/National Supply Company).

They noted differences in machinery finance as well. In the U.S., the OEMs and banks appear to have a lot of leverage in financing. Brazil, meanwhile, relies greatly on public financing. The cost of money is another factor, they said.

They also recognized the subsidized advantages the U.S. government provides that reduces risk.

Use of the Products

The use of the machinery is also different, with longer use and financing periods.

The machinery use, and thus, the updates in the renewal of the fleets, is a longer cycle in the U.S. The machinery is used for longer hours in Brazil because it’s used across much larger areas, and generally doubled because of the 2 harvests. For instance, they said a combine may work 3-5 times more hours in a year in Brazil than its counterpart in the U.S.

The pre-owned sales market in Brazil is not as mature as it is in the U.S.

Dealer Facilities

The dealers perceive a higher value placed on the dealer’s infrastructure in Brazil. Things like the look and feel of the store, its size, cleanliness and maintenance, and even how the personnel are dressed — as well as all visual and comfort aspects— are highly valued and expected by the customer in Brazil.

In the U.S., meanwhile, the dealers perceived that the facility is a desire of the owner of the store, not a demand made by the farm customer.