It may be strong and stable in the near term, but we have longer-range concerns

Although sales growth in the United States and Canada is likely to remain sluggish this year, the management teams Deere, CNH and AGCO share a sense of optimism for the near term. However, we're still concerned the medium-run prospects for farm equipment manufacturers in North America could face headwinds stemming from reduced farm income and difficult year-over-year comparisons. Growth in emerging markets, like Russia, should lead to solid returns for the firms, but likely weakening in South America (due to recent droughts) and potentially Europe (stemming from economic headaches) further tempers our enthusiasm. We don't believe the market is currently offering a suitable margin of safety for these stocks, though we'd keep an eye on narrow-moat-rated Deere.

The total North American tractor and combine market climbed about 2% in 2011, and AGCO and CNH expect continued single-digit gains in 2012. However, Deere increased its forecast to 10% growth after its first-quarter report. Cash crop receipts will probably remain healthy this year because of lofty commodity prices, but we believe double-digit growth is a bit aggressive, given a potential flattening of crop receipts, higher input costs (such as fertilizer) and difficult comparisons in the high-horsepower market.

Much of this outlook hinges upon the year's global weather performance. A continued drought in southern Brazil and Argentina could crimp corn and soybean yields in the region, likely putting upward pressure on worldwide prices of the commodities. Conversely, a bumper U.S. crop as a result of favorable weather conditions could reduce prices more than the increased harvest amount, limiting farm income growth. Over the longer term, we believe a return to better weather conditions will eventually lead to a negative year for the farm original-equipment manufacturers, although it's nearly impossible to pinpoint the exact timing. That said, we were pleased to hear the Midwest's snowfall melt-off only contributes about 10% of the region's annual moisture; a few solid spring rains would overcome this year's snow shortfall.

All three manufacturers have announced sizable price increases, which should offset increasing raw-material costs and heightened expenses related to Tier 4 interim engine updates. Given the decent barriers to entry in this market, we expect the OEMs to fully pass through these announced increases.

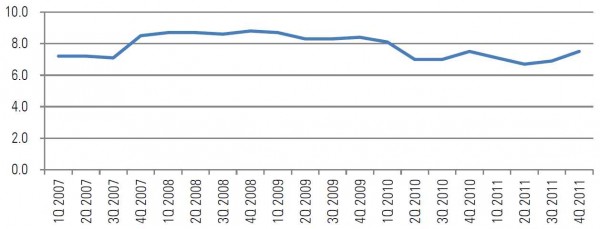

Used Combine Inventory Better, but Bears Watching

Manufacturers believe used combine inventories have improved, and a recent industry measurement of equipment values seems to bear out this thinking. However, we remain concerned about the recent drop-off in this product line year-over-year.

Easing our qualms, we point to used values for these combines, which have increased in recent months. We follow Machinery Pete's index of used equipment values, which measures industry consultant Greg Peterson's observed pricing at equipment auctions around the country. A "6" rating suggests normalized demand. As seen in the chart below, used combine values declined sharply from 2009 levels through 2010 and 2011, likely indicative of the overhang of machinery in the marketplace. However, this metric ticked up in the fourth quarter, suggesting a sharply reduced supply of used equipment.

Machinery Pete's Combine Harvester Used Value Index, Quarterly 2007-11

Although used values for combines have improved and tractor used values remain red hot, the fleet age is probably very young for both combines and high-horsepower tractors, which could be problematic in several years as these machines move into the used market. When combined with eventual lower farmers' cash receipts, we expect farm equipment OEMs to continue to see boom and bust years in their businesses.

Technology Still an Important Strategy

With slowing growth, OEMs are trying to woo customers with valued-added technology. For example, Case IH and Deere are trying to allow more communication with third-party providers within their systems. We think this is a positive step for farmers, who will be able to let agronomists, seed producers and other vendors examine farm-specific data to increase yield and productivity. New apps for smartphones and tablets will also allow farmers to view real-time data and analyses throughout the day.

This side of the business received a boost from the Federal Communications Commission's recent decision to revoke LightSquared's provisional approval to build out a nationwide mobile broadband service. GPS device manufacturers, including those in the farm industry, had complained that the planned technology would have interfered with signal quality, and the FCC seems to agree. Although not a valuation driver in our discounted cash flow models, we think the ruling lifts potential uncertainty from the customer's point of view.

Equipment manufacturers will also continue to offer new engine technologies throughout the year (as required by Environmental Protection Agency mandates), although many will use engine credits to manage the timing of these products, given the plant shutdowns required to manufacture the updated models. We think AGCO and CNH - which opted for selective catalytic reduction rather than exhaust gas recirculation engine technology - could continue to enjoy some share gains, as their updated models' fluid efficiency is now on par with Deere's. We had originally expected research and development spending to decline in coming years for these firms, but CNH has specifically said it intends to maintain its high R&D spending level, albeit toward machine development rather than primarily for engines.

Stocks Look Fairly Valued

International growth in Russia and parts of Europe could help to offset slowing North American sales over the near term, and Deere in particular has made recent successful product pushes in Brazil and Europe. However, we expect global unit volume for tractors and combines to be roughly flat in 2012. We think positive pricing actions will lead to decent top-line growth for all three OEMs we cover, but we remain concerned regarding gains in outer years because of industry cyclicality and eventual difficult year-over-year comparisons. We also foresee mid-cycle operating profitability at around current levels; each firm is likely to continue to enjoy near-term margin expansion while sales rise further, but we expect income to fall sharply in years of declining cash receipts, given the companies' high degree of fixed costs. In all, we think Deere, AGCO and CNH are currently about fairly valued.

Our fair value estimates imply roughly mid-teen price/earnings multiples to our estimated mid-cycle earnings per share assumptions, about in line with historical trading ranges; we think recent forward multiples around 10 times suggest the market also expects some earnings degradation. Nonetheless, we wouldn't hesitate to recommend best-in-class operator Deere at the right price, as we doubt a farming downturn would permanently dent the firm's market position.

Reprinted with Permission