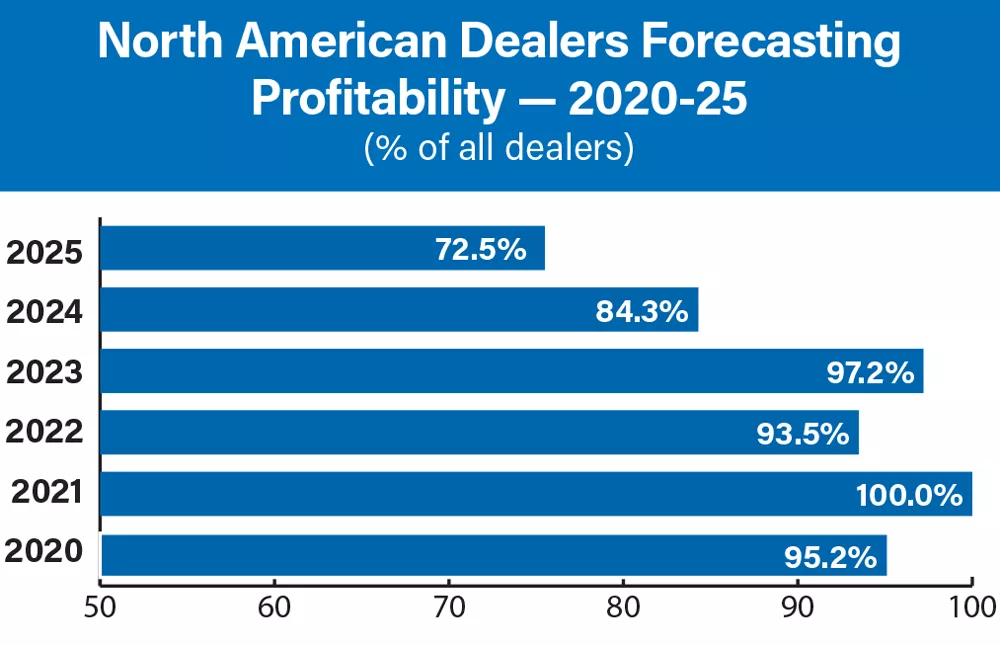

Trade disputes, the rising cost of equipment, high interest rates and low commodity prices made for a challenging year for farm equipment dealers in 2025. According to the 2026 Dealer Business Outlook & Trends survey, 72.5% of dealers expected their business would be profitable in 2025, a 6-year low. And from the looks of it, 2026 is likely to be another challenging year as the industry closely watches to see if we’re at the bottom of the trough.

New equipment sales were a challenge for dealers and manufacturers alike in 2025, with large ag equipment sales down 26.5% through October, according to the Assn. of Equipment Manufacturers. While dealers are forecasting another challenging year, there have been improvements in their outlook.

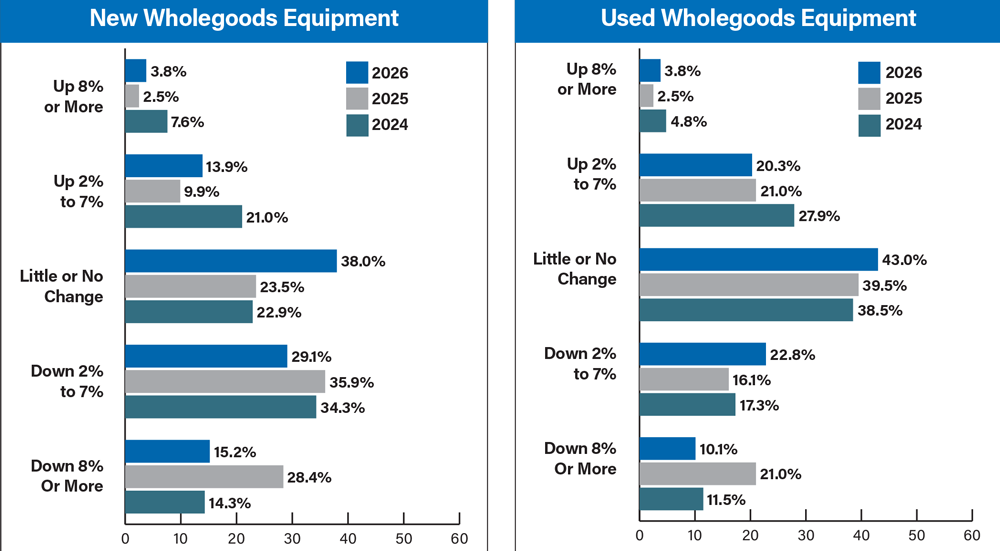

While over 44% of dealers are forecasting new equipment sales to be down at least 2% in 2026, more dealers are calling for flat sales or sales growth than in 2025.

Nearly a third of dealers are forecasting used equipment sales to be down vs. 2025, but a higher percentage (67.1% vs. 63.0%) say sales will be as good or better than last year.

Dealer & Farmer Sentiment

Dealer and farmer sentiment continued to remain low through much of 2025, as it has for the previous 3 Dealer Business Outlook & Trends reports. Much like in the 2024 and 2025 reports, dealer sentiment has been low throughout the year due to declining sales, high interest rates and increasing costs of equipment. In fact, the latest Dealer Sentiments & Business Conditions Report from Ag Equipment Intelligence shows that dealer optimism was at — 38 in October 2025. At the start of 2025, the optimism reading was at — 15, the highest reading of the year.

In the latest report, one dealer commented that its 2026 orders are tracking at a 5-year low.

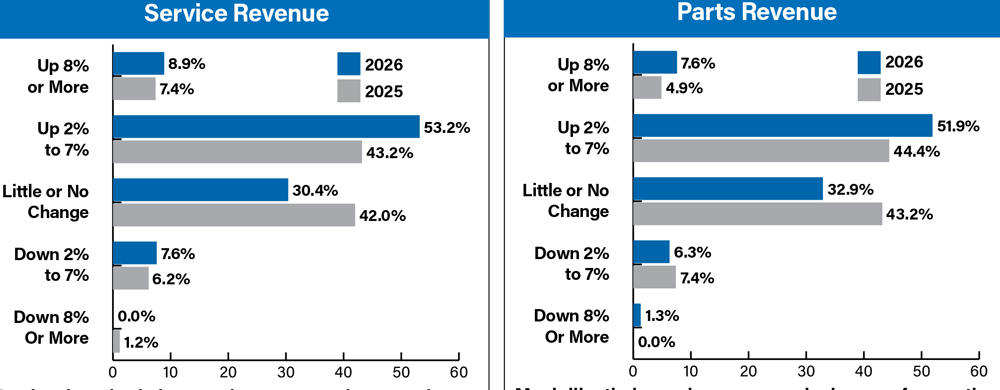

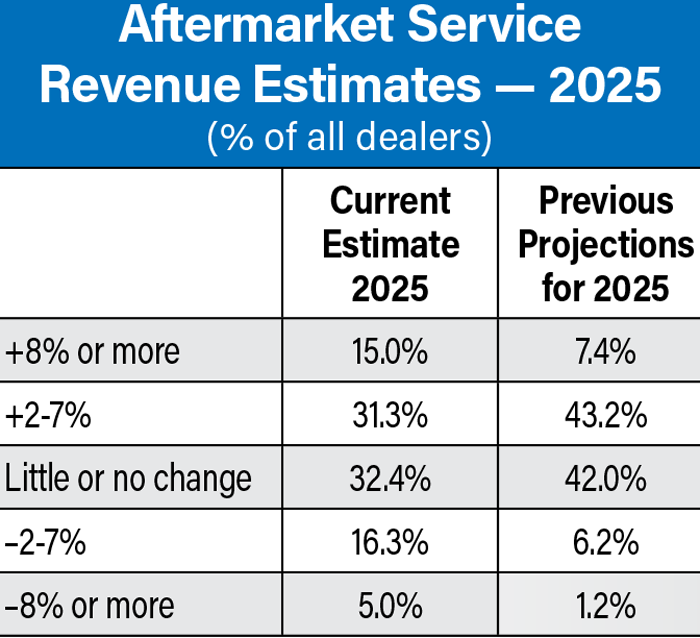

Dealers’ outlook for service revenue improved over 2025, with 62.1% of dealers forecasting service revenue to be up 2% or more vs. 50.6% in 2025.

Much like their service revenue, dealers are forecasting parts revenue growth in 2026, with nearly 60% of dealers expecting parts sales to be up 2% or more vs. 2025.

One Canadian dealer commented, “The tariffs could pose a problem to farmers well into 2026 and will create inflationary pressures not only on equipment but on several inputs and parts maintenance. We tried to buy a piece of used equipment and the cost rose ~$25,000 following tariff surcharges.”

As it relates to trade, one corn belt dealer said, “The soybean trade deal with China could help farmers come closer to break even, however, we think we need to see a 10% boost in grain markets vs. current rate to start to see an uptick in equipment sales.”

Farmer sentiment, on the other hand, has been up and down throughout the year. The latest Purdue University-CME Group Ag Economy Barometer Index climbed to 139 in November 2025, 10 points higher than in October and the highest barometer reading since June 2025. The improvement in farmer sentiment was attributable to producers’ more optimistic outlook for the future, as the November Future Expectations Index reading of 144 was 15 points higher than in October, whereas the Current Conditions Index fell 2 points to a reading of 128. This month’s survey was the first survey conducted since the late October announcement of a trade pact between the U.S. and China that included provisions for increasing U.S. exports of agricultural products to China, and survey respondents were notably more optimistic about future prospects for U.S. agricultural exports. Sentiment was also buoyed by a sharp rise in crop prices from mid-October to mid-November.

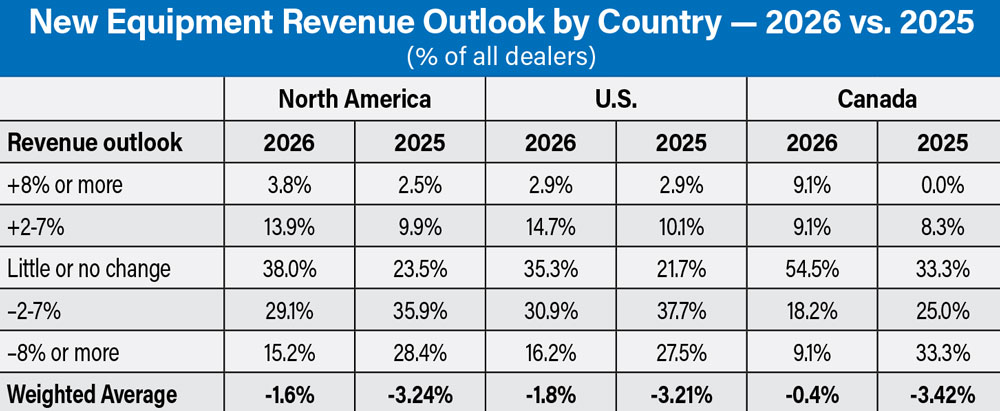

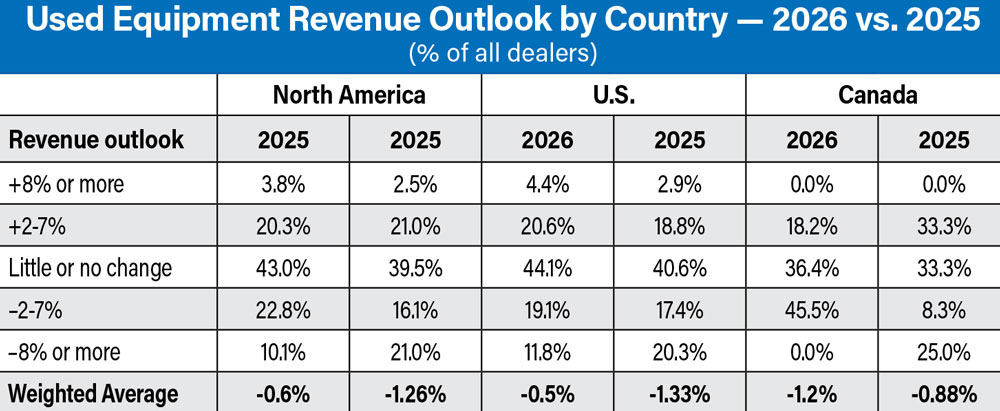

Across the board dealers are more optimistic about their new equipment revenue in 2026 compared to 2025, and Canadian dealers are more optimistic than their U.S. counterparts.

Inventory Management

Dealers’ new and used equipment inventories remained elevated through much of 2025. The latest Dealer Sentiments report showed a net 42% of dealers said their new equipment inventory was too high (46% too high, 50% inline, 4% too low), while a net 27% said their used equipment inventory was too high (40% too high, 46% inline, 13% too low).

However, when it comes to dealers’ top concerns, inventory remains in the middle of the pack and in fact came in lower on the list than the last couple of years. Dealers ranked new equipment inventory #15 (down from #12 last year) and used equipment inventory #16 (down from #14 last year).

Dealers and OEMs alike have put a focus on lowering their inventory. In fact, Titan Machinery reported it had shed 28.5% of its inventory year-over-year by the end of its third quarter.

More U.S. dealers expect used equipment revenue growth (25.0%) than Canadian dealers (18.2%) in 2026. Last year, Canadian dealers who were more optimistic.

Commenting on the results in a note to investors, Baird analyst Mircea (Mig) Dobre noted that Titan reported good destocking progress and said “used inventory reduction is notable, lowering the risk of write-downs.”

Total inventories fell by $129.3 million sequentially, or by 11.3%, to $1.011 billion (–28.5% year-over-year). “Equipment inventories (down 32% year-over-year) have been reduced by $98 million through 9 months; notably, used inventories have been reduced by $96 billion, which is important since used inventories carry the highest write-down risk,” he wrote. “Management upped its equipment inventory reduction target to $150 million for FY26 (previously $100 million).”

“We need to see a 10% boost in grain markets vs. current rate to start to see an uptick in equipment sales…”

The OEMs adjusted production levels to help address high inventories. In Deere’s Q4 2025 earnings call with investors, Josh Beal, director of investor relations, said, “This year’s results also reflect focused cycle management, most notably in managing inventory. In North America large ag, we produced roughly in line with retail demand for the full year, keeping new field inventory at the very low levels where fiscal 2025 started. Inventory to sales ratios for combines and 4WD tractors both closed the year at 8%, while 220 horsepower and above tractors were at 12%. To put in perspective how low absolute inventory levels are, new field inventory for Deere 220 horsepower and above tractors ended fiscal 2025 at the lowest unit level we’ve seen in over 17 years.”

In AGCO’s Q3 2025 earnings call, CEO Eric Hansotia said the company had made “meaningful progress” in reducing its North American dealer inventory from 9 months to 8 months during the third quarter. However, he noted that it is still above AGCO’s target. “The reduction reflects the success of our disciplined production cuts with units being reduced almost 13% in the quarter,” he said.

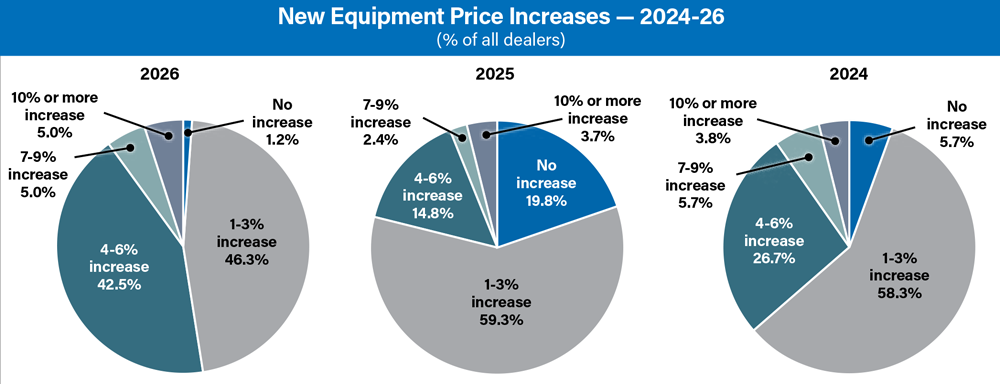

The percentage of dealers who say they expect their mainline OEM to raise prices 4-6% nearly tripled compared to 2025. However, the largest percentage of dealers once again are anticipating an increase of 1-3, similar to 2025 and 2024.

2026 Wholegoods Outlook

The majority of dealers are forecasting 2026 new equipment revenue to be down to flat. However, the percentage calling for flat sales in 2026 grew compared to 2025 (38% vs. 23.5%), which also translates to an improvement in the percentage expecting sales to improve in the year ahead.

Nearly 18% of dealers are expecting 2026 new equipment revenue to be up at least 2% vs. 12.4% forecasting the same level of growth for 2025. The percentage of dealers forecasting revenues to be down 8% or more dropped to 15.2% vs. 28.4% in 2025. The percentage of dealers calling for new equipment revenues to be down 2-7% dropped by nearly 7 percentage points to 29.1%.

Dealers’ outlook for used equipment revenues is similar to their outlook for new equipment, but with a higher percentage (24.1%) calling for an increase of at least 2% or for sales to be flat (43%) vs. 2025. Nearly a third of dealers, however, are forecasting their used equipment revenues to be down vs. 2024.

Dealers' 2025 Revenue Estimates vs. Forecasts

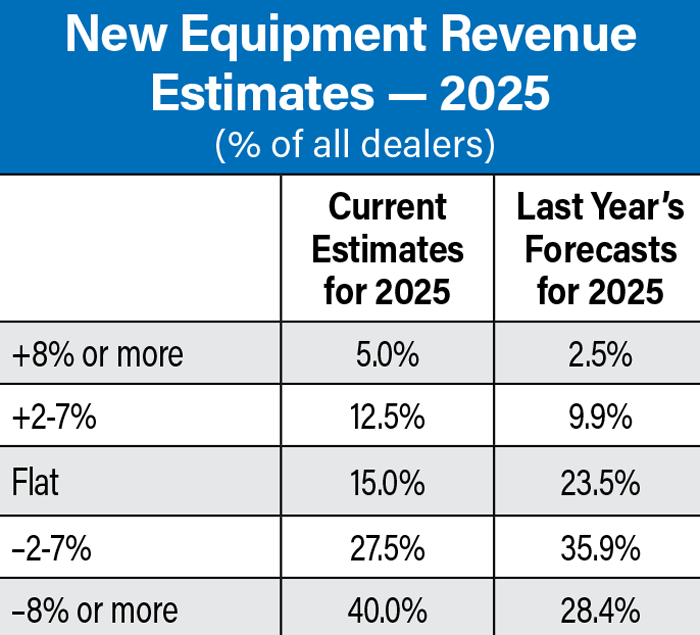

The results of 2026 Dealer Business Outlook & Trends survey show over two-thirds of dealers are reporting their revenue from new equipment sales will be down vs. 2024, largely in line with their forecast from a year ago.

While the total percentage of dealers reporting their new equipment revenues would be down in 2025 remained fairly even with what dealers forecast for 2025 a year ago, there were shifts in how much of a decline they expected. For example, a year ago just over 28% of dealers forecast their new equipment revenue to be down 8% or more. That number grew 11.6 percentage points to 40% of dealers now saying their 2025 new equipment revenues will be down 8% or more compared to 2024. On the flip side, there was some improvement in dealers reporting revenue growth.

Across the board, dealers forecasts a year ago were off from what they are seeing today, most notably the percent of dealers reporting new equipment revenue was down 8% or more increased by 11.6 points vs. a year ago.

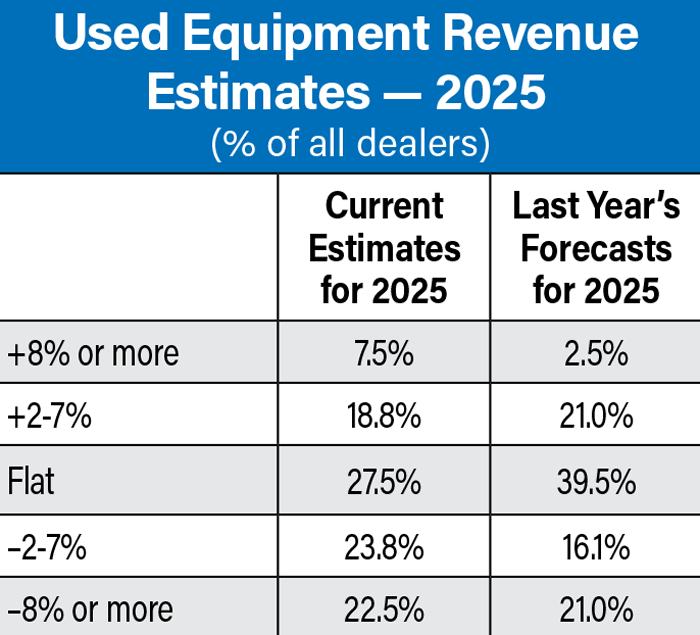

On the used equipment side of the business, the percentage of dealers reporting 2025 revenues increased by at least 2% vs. 2024 increased by about 3 percentage points compared to what dealers were forecasting for 2025 when surveyed a year ago. However, the percentage of dealers reporting a decline of 2% or more (46.3%) vs. 2024 was also up compared to the forecast from a year ago (37.1%).

The percent of dealers reporting used equipment revenue growth in 2025 was up (26.3%) compared to forecasts made a year ago (22.5%). However, it was up for revenue declines as well (46.3% vs. 37.1% a year ago).

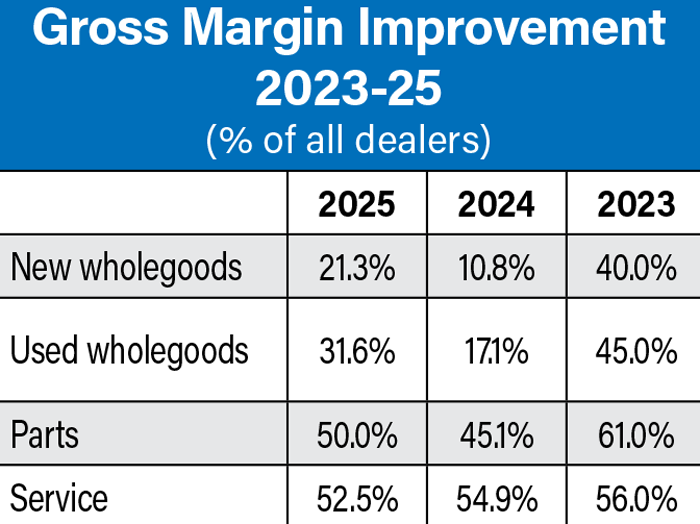

Looking at the aftermarket business, a year ago nearly half of dealers were forecasting parts revenue to increase over 2024 with another 43.2% of dealers calling for flat sales. In the latest survey, the percentage of dealers reporting an increase over 2024 fell to 45% and the dealers who are reporting flat revenues dropped to 32.5%.

The percentage of dealers reporting improvements in their gross margins was up year-over-year in all categories except service.

A year ago, only 7.4% of dealers expected parts revenues to be down in 2025 compared to 2024. Today, 22.5% of dealers are reporting their parts revenue is down at least 2% vs. 2024.

During the 2025 Executive Briefing Mid-Year Review in June, H&R Agri-Power President Steve Hunt commented that the Case IH dealership group’s parts sales were facing headwinds, which was something the group had not anticipated.

“I don’t know if the fleet’s new enough or not, but we’re down single digits there year-over-year and single digits to our budget,” he said.

While the majority of dealers parts revenue was up in 2025 vs. 2024, dealers didn’t quite hit their estimates from a year ago.

More dealers reported service revenues were down vs. 2024 (21.3%) compared to what was predicted a year ago (7.4%).

“We’re not too far off the budget. We projected to be down some, but service sales, likewise, were the same trends in parts and service, which do not fare well with our absorption rate.”

Service revenues have also seen a shift from dealers predictions a year ago vs. their current estimates. Last year, 50.6% of dealers were calling for service revenues to be up at least 2% vs. 2024.

Today, 46.3% of dealers expect that same level of improvement in service revenues over 2024. The percentage of dealers expecting service revenues to be down vs. 2024 went up to 21.3% in the latest survey from 7.4% a year ago.

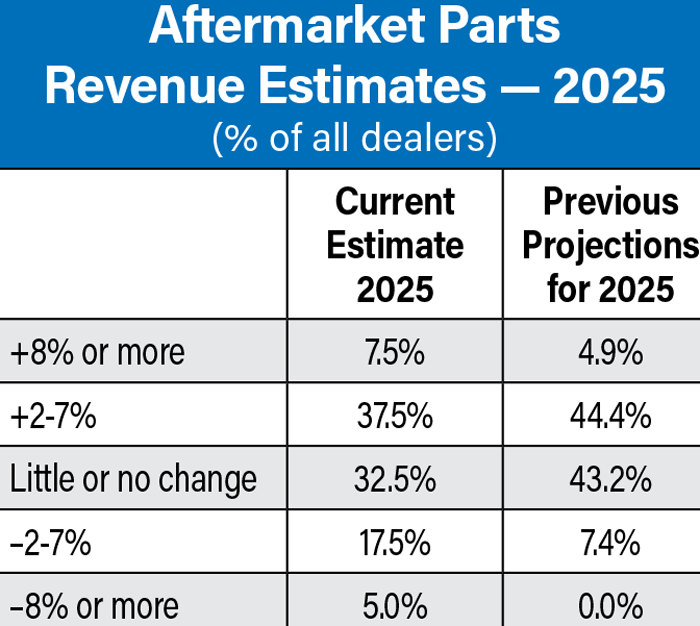

Much like 2025, dealers are the most optimistic about their aftermarket revenues with nearly 60% of dealers forecasting 2026 parts revenues to be up over 2025 and another third of dealers expect flat parts revenues. According to dealers’ forecasts, service offers the greatest opportunity for increased revenues with 62.1% of dealers calling for revenues to be up at least 2% in 2026.

Equipment Prices & Early Orders

Nearly all the responding dealers are expecting a price increase from their mainline supplier in 2026, with just 1.3% saying no. The largest percentage of dealers are expecting an increase of 1-3% (46.3%) and 4-6% (42.5%).

Still, 5% of dealers reported a price increase of 7-9% and another 5% are expecting to see an increase of 10% or more.

The majority of dealers once again are reporting early orders are down compared to the previous year. Just 7.6% of dealers said their early orders were up, which is an improvement from less than 5% in 2025 but still down from 15% in 2024. Almost a third of dealers (31.3%) said their 2026 early orders were about the same as last year vs. 17.1% who said the same about 2025.

In terms of how much dealers reported orders were down, 27.5% said their orders were down 10% or more. Nearly 14% reported their early orders were down 6-10% vs. 2025 and another 20% said they were down 1-5%.

Tractor & Combine Sales

Overall, dealers aren’t particularly optimistic on their outlook for high horsepower tractor and combine sales, however for both categories the highest percentage of dealers are forecasting flattish sales (44.6% and 40.5%, respectively).

For tractors over 100 horsepower, 35.1% of dealers forecast their unit sales to be down in 2026 vs. 2025. Of that, 21.6% expect unit sales to be down 2-7% and the other 13.5% expect sales to be down 8% or more. On a positive note, just over 20% of dealers are forecasting an improvement in 100-plus horsepower tractor unit sales of at least 2% over last year.

When it comes to utility tractors (40-100 horsepower), dealers are more optimistic, with 25.7% forecasting unit sales to be up at least 2% in 2026 and another 58.1% expecting sales to be flat compared to 2025.

For combines, 47.9% of dealers are calling for unit sales to be down at least 2% (vs. 63.1% last year) with just over 11% expecting sales to be up 2% or more compared to 2025 (vs. 7.7% last year).

Best Bets for Increasing Sales

Each year dealers are asked to provide their unit sales projections for a number of product categories. Those projections are used to determine dealers’ best bets for improving sales in the year ahead. For the third year in a row, precision farming equipment & technology topped dealers’ list of best bets for improving unit sales, with 88.24% of dealers forecasting sales to be as good or better than 2025.

With grain prices continuing to remain low, dairy provides a bit of optimism for equipment sales for dealers and manufacturers alike. The “best bets” list confirms that livestock and dairy customers will provide opportunities for dealers in 2026, much like this year. Coming in at No. 2 is feeders/mixers (87.5%) and at No. 3 forage harvesters (86.2%). Both were in the top 5 last year, but it should be noted that for each product, over 70% of dealers are anticipating sales will be flat.

“The service department continues to be an area dealers plan to invest…”

Rounding out the top 5 is lawn & garden equipment at 86.1%, which jumped from No. 7 in 2025 to No. 4, and farm loaders at 85.7%, which jumped from No. 11 last year to No. 5. Utility and compact tractors both made it into the top 10 at No. 7 and No. 9, respectively.

Coming in the bottom of the list were 2WD tractors over 100 horsepower, 4WD tractors and combines. Pull-type sprayers fell from No. 8 on the list in 2025 to No. 12, while self-propelled sprayers jumped 1 spot from No. 14 in 2025 to No. 13 in 2026.

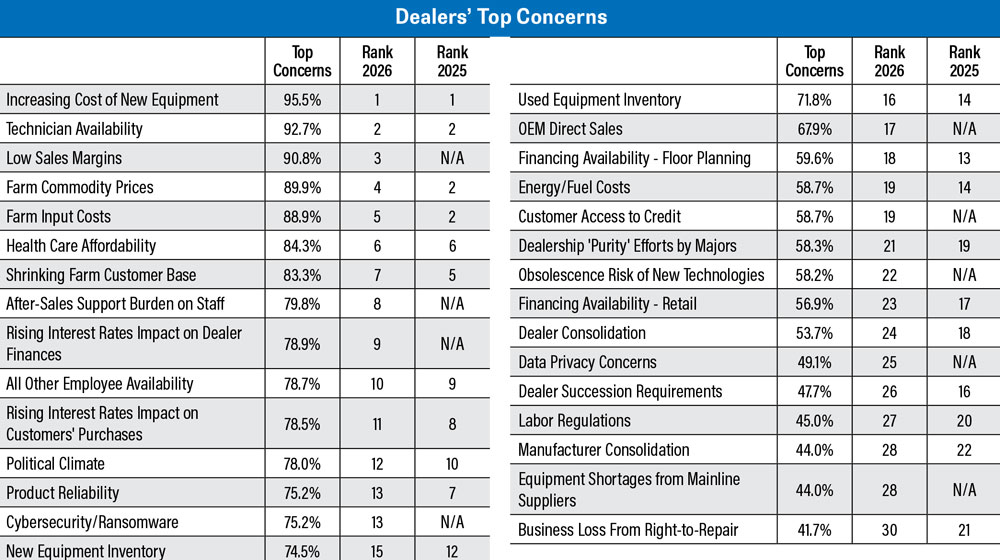

The increasing cost of new equipment continues to be the top concern for farm equipment dealers, followed by technician availability. Low sales margins was added to the options dealers could select this year and it made its debut high on the list at No. 3. Financing availability — retail fell from No. 17 in 2025 to No. 23 in 2026.

Top Concerns

For the second year in a row, the increasing cost of new equipment topped dealers list of concerns, with 65.5% of dealers saying it was the issue they were most concerned with and another 30% marking “concerned.” Since 2022, the cost of equipment has bounced between No. 1 and No. 4 on the list.

As has been the case for the last several years, technician availability took the No. 2 spot of dealers top concerns, with 63.3% ranking it as “most concerned” and 29.4% saying they were concerned.

New on the list this year — and coming in at No. 3 — was low sales margins with 90.8% of dealers saying they were either most concerned or concerned. Rounding out the top 5 were farm commodity prices and farm input costs, which were tied for No. 2 on the list of top concerns in 2025.

Hiring & Investment for 2026

With the exception of service technicians, dealers are largely looking to keep staff sizes the same. That said, more dealers say they will add staff than reduce or reallocate staff.

For service techs, 63.5% of dealers plan to add staff, with about a third saying they’ll make no changes to their staffing in the service department. In the parts department, just over 56% of dealers plan to make no changes, but just shy of 39% of dealers intend to add to their parts staff.

When it comes to wholegoods sales, 38.6% of dealers intend to add staff with another 54.2% planning no changes to their sales staffing.

“The ‘best bets’ list confirms livestock & dairy customers will provide opportunities for dealers in 2026…”

In terms of capital expenditures, over half of dealers (53.4%) plan to increase their spending to some degree in 2026, with the most (41%) planning to increase their capital spending by up to 5%.

The service department once again had the highest percentage of dealers saying they would invest in modernizing their shop at 51.9% vs. 31.7% in 2025. Another 47.7% said they would increase their spending on mobile service vehicles compared to 30.3% in 2025.

And 41.5% said they would be investing in business information systems, up for 30.3% last year.

Showroom improvements had the lowest percentage of dealers who were planning to invest there at 29.2%, but that is up from 15.8% in 2025.

The full 2026 Dealer Business Outlook & Trends Report is available on Ag Equipment Intelligence.