Using a financial model and not just a budget is important to achieving consistent profitability. To show the difference between the two, let’s consider a real world situation for a dealership.

Suppose that in the fall of 2010 you built a budget for 2011, which, based on a good economy and increased customers demand, looked pretty good at the time. But now, several months into 2011, your budget and reality are not in sync. What should you do to correct this and better monitor and control your business?

Budget vs. Reality

Let’s assume that your sales manager designed his 2011 budget to produce a 15% gross profit with expenses of 12%. That might have sounded pretty good late last year, but this year has been tougher than expected. Competitors have been aggressive and your sales margins are tighter than planned because you agreed to do what was needed to maintain your market share. So, the result is a gross profit margin year-to-date of 13.5% — well below the budget of 15%.

So if the margins are down but you’re still maintaining your original budgeted sales volume and budgeted expenses, things should be okay, right?

Wrong! Your net profit in the sales department is half of what you planned.

What happened? Your original forecast of 15% gross profit minus expenses of 12% would have produced a 3% net profit. Now, your actual margin of 13.5% less the 12% of expenses is only 1.5% — one-half of what you budgeted. To maintain your profit, you only have two choices — increase revenue or reduce expenses.

Using a Financial Model

If a financial model was used for planning and controlling this same sales department, you would likely reduce expenses — almost automatically.

How is a financial model different?

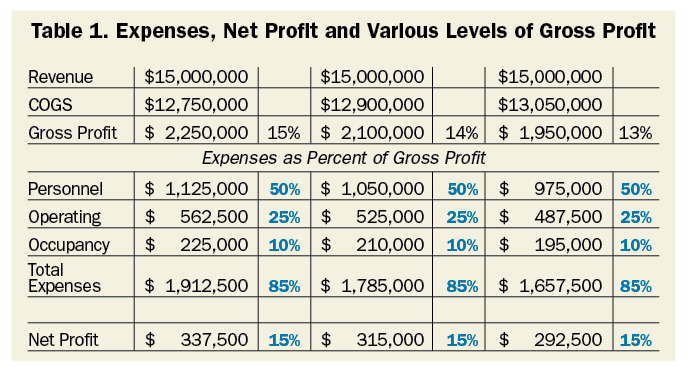

In the financial model the benchmarks (expected performance ratios) are all percentages of the gross profit dollars in the sales department as shown in Table 1.

This way of looking at expenses changes your view from static budget numbers to a dynamic adjustment to reality. By reducing expenses as gross profit margin decreases, net profit margin in maintained. This is one of the most powerful techniques of using a financial model. Of course, reducing expenses is easier said than done. But a financial model tells you when you should adjust and by how much.

Aftermarket Financial Model

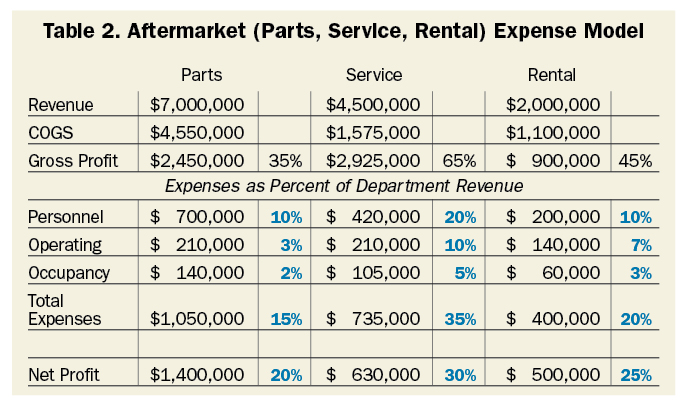

When working with the product support or aftermarket departments (including rental), we can base expenses on total revenue because maintaining the gross profit margins in these departments is typically simpler than with wholegoods. The financial model for these departments is shown in Table 2.

From these elements of a financial model we can start to figure out how much we could or should be spending for wages and benefits for employees in each department, as well as operating and occupancy expenses. This is helpful because we have set expectations for expenses for each department. Issues, such as service vehicle recover, can and should be measured so we can control individual expenses for the service department.

G&A Expense Modeling

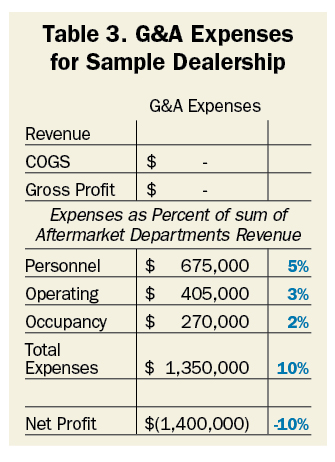

Looking at the table for parts, service and rental, you may say that the bottom numbers (% net profit) are higher than a dealership can expect. But we have not yet considered the next element of the financial model, which are the general and administrative expenses, or what some people call fixed expenses.

These are the expenses that the dealer principals and general managers decide on spending to run the dealership. Examples are the compensation of the accountant, payments to the lawyer and other compensation and benefits to owners. These are expenses that the parts or service managers cannot determine. They can’t fire the accountant, owner or select a lawyer. Therefore, these expenses are all grouped into G&A expenses and are separate from departmental profit and loss statements.

In this model, these expenses are determined based on the revenue of the aftermarket departments. Using the information in Table 2, total sales of parts, service and rental are $13,500,000. This means our G&A expenses would be as follows:

Why is the sales or wholegoods department calculated on gross profit? Why are G&A expenses based on the total revenues of the aftermarket departments?

The answer is the same. We believe that the wholegoods sales department should stand on its own and be able to generate enough profits to consistently cover their costs even when the market is slow. The focus on the aftermarket establishes the proper balance in a dealership and helps to create the proper perspective and information to help drive full absorption.

Putting It Together

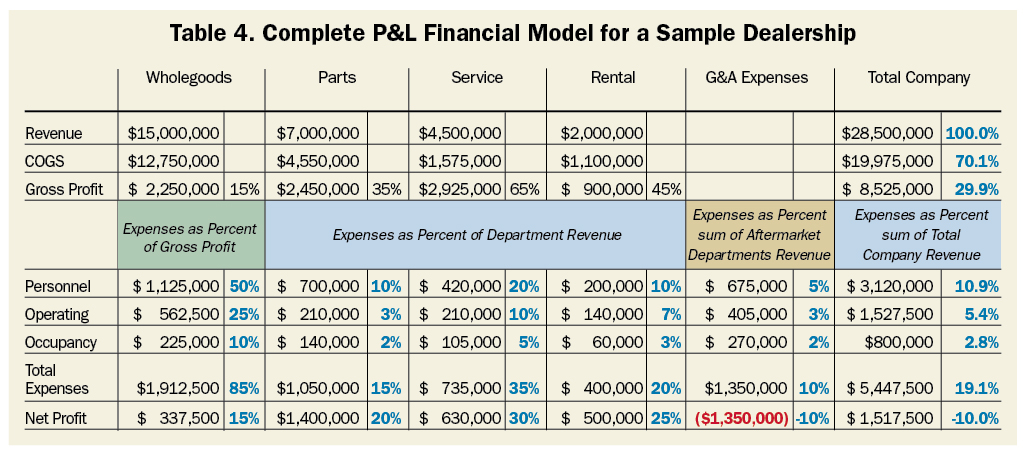

All of the these various elements are combinded to produce the Complete P&L Model for a Sample Dealership shown in Table 4.

We have used this method of financial modeling with over 400 dealers, but there are other methods. The point is to distinguish between a budget and a financial model. Doing so will help you to more consistently Plan your Profits.

The authors are with Currie Management Consultants who specialize in advising dealers in the machinery industry. The can be reached at GRussell@CurrieManagement.com and GKeen@CurrieManagement.com.