In issuing its second quarter earnings report, CNH Industrial reported the following:

- Consolidated revenues were $4.7 billion on lower industry demand

- Results reflect continued execution of cost saving initiatives partially offsetting market headwinds

- Full-year guidance reaffirmed

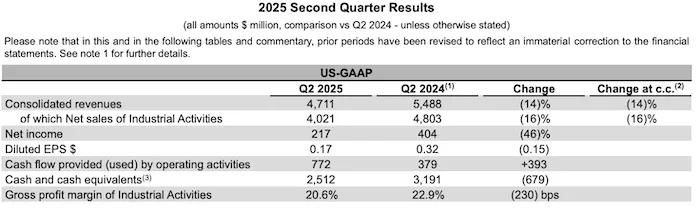

CNH Industrial, reported on Aug. 1 results for the three months ended June 30, 2025, with net income of $217 million compared with net income of $404 million and for the 3 months ended June 30, 2024. The company also reported that consolidated revenues were $4.71 billion (down 14% compared to Q2 2024), and net sales of Industrial Activities were $4.02 billion (down 16% compared to Q2 2024). Net cash provided by operating activities was $772 million, and Industrial free cashflow was $451 million in Q2 2025.

“While we continued to face challenging market conditions this quarter, the CNH team's resilience and dedication allowed us to navigate through them effectively and in line with our targets, says Gerrit Marx, Chief Executive Officer. “We are focused on the strategic priorities that we outlined at our recent investor day to advance our operational improvements and the investments that deliver exceptional products and technology for our farmers and builders. We appreciate the support from our suppliers as we navigate uncertain trade waters, and from our dealer network that strives for unmatched customer service as we position CNH for long-term success. I am excited for the future of CNH and sharing the journey ahead with you.”

The decline in net sales of Industrial Activities was mainly due to lower shipments on decreased industry demand and continued dealer destocking.

Adjusted net income was $216 million. In comparison, Q2 2024 adjusted net income was $451 million. Income tax expense was $76 million ($95 million in Q2 2024), and the effective tax rate (ETR) was 27.6% (20.9% in Q2 2024) with an adjusted ETR(4) of 27.7% for the second quarter (21.0% in Q2 2024). Cash flow provided by operating activities in the quarter was $772 million ($379 million provided in Q2 2024). Free cashflow of Industrial Activities was $451 million, a year-over-year improvement of $311 million due to lower net change in working capital.

Source: CNH Industrial

In North America, industry volume was down 7% year-over-year in the second quarter for tractors under 140 HP and was down 37% for tractors over 140 horsepower; combines were down 23%. In Europe, Middle East and Africa (EMEA), tractor demand was down 7%, while combine demand was up 8%. South America tractor demand was up 4%, while combine demand was down 6%. Asia Pacific tractor demand was up 3%, but combine demand was down 42%.

Agriculture net sales decreased in the quarter by 17% to $3.25 billion vs. the same period of 2024, primarily due to lower shipment volumes on decreased industry demand and dealer destocking.

Adjusted EBIT decreased to $263 million ($502 million in Q2 2024) driven by lower shipment volumes, partially offset by favorable net price realization and lower production, warranty and SG&A expenses. R&D investments accounted for 6.0% of sales (5.5% in Q2 2024). Adjusted EBIT margin was 8.1% (12.8% in Q2 2024).

2025 Outlook

The Company continues to forecast that 2025 global industry retail sales will be lower in both the agriculture and construction equipment markets when compared to 2024. CNH is still focused on driving down excess channel inventory primarily by producing fewer units than the retail demand level, which will result in 2025 net sales being lower than in 2024.

The lower production and sales levels will negatively impact our segment margin results. However, the Company’s ongoing efforts to reduce its operating costs will partially mitigate the margin erosion. CNH is continuing its focus on product cost reductions through lean

manufacturing principles and strategic sourcing. The Company is also carefully managing its SG&A and R&D expenses.

In addition to the lower cyclical industry sales, the Company is navigating a changing global trade environment. The uncertainty of the U.S. trade policy, the reactions of trading partners, and the impact to our end customers may affect our forecast for the year.

The Company is reaffirming its previous 2025 outlook:

- Agriculture segment net sales down between 12% and 20% year-over-year, including -1% of currency translation effects

- Agriculture segment adjusted EBIT margin between 7% and 9%

- Construction segment net sales down between 4% and 15% year-over-year, including -1% of currency translation effects

- Construction segment adjusted EBIT margin between 2% and 4%

- Free cash flow of Industrial Activities(6) between $100 million and $500 million

- Adjusted diluted EPS(6) between $0.50 to $0.70

Click here for more Industry News.