Rabobank doesn’t see sales of ag equipment picking up until possibly 2018. In the meantime, one of agriculture’s largest lending institutions thinks the time could be right for some of the bigger farm machinery manufacturers to get together to challenge market leader John Deere.

According to the September 2015 report, “Contraction Today, Consolidation Tomorrow? Looking Beyond the Downturn in North American Farm Equipment,” the ag lender concludes that the downturn in farm equipment sales that has carried over into 2015 “is unlikely to abate for some time.”

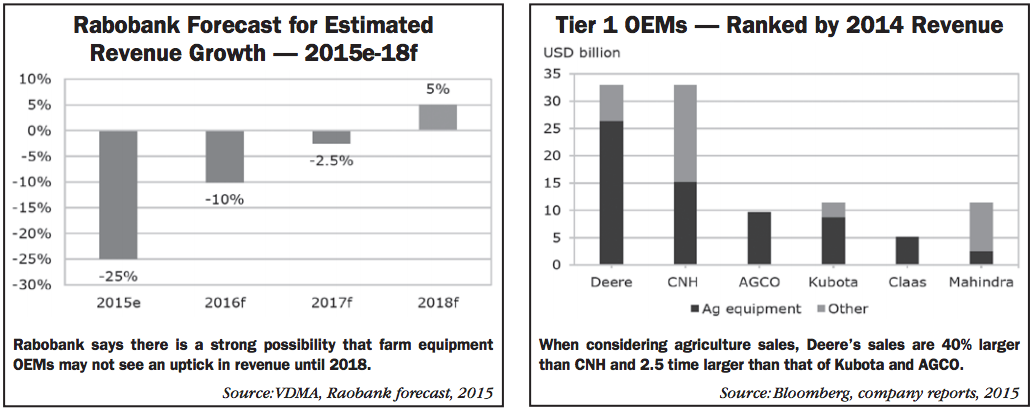

The report, authored by Ken Zuckerberg and Harry Smit, contends that despite recent sales uptick for small tractors, “the overall operating environment for OEMs of farm equipment and machinery remains quite ominous.” The ag lender projects “North American revenues derived from the sales of tractors and combines will likely fall by 25% in 2015, 10% in 2016 and 2.5% in 2017, with the inflection point for positive growth of about 5% occurring in 2018.”

The current oversupply of used equipment must be worked down before dealers will increase their delivery of new equipment from the OEMs.

According to the Rabobank researchers, the current downturn could set the stage for “disciplined competitors to consider strategic mergers and acquisitions that will grow market share, diversify product offerings, enter adjacent markets and expand in higher growth regions.”

In citing the potential for consolidation by equipment OEMs, the report cites recent merger and acquisition activity within the farm input subsector of agriculture. These include Monsanto’s bid for Syngenta, FMC’s acquisition of Cheminova and the recent merger agreement between CF Industries and OCI.

In 2014, it is estimated that farm equipment was a $114 billion industry, with $26 billion of this coming from sales in North America. Revenue and unit sales growth was 9.9% and 5.8%, respectively from 2010-2014. Even at this size, the report says the ag equipment sector is still second to the global farm inputs sector, which is dominated by fertilizer at $175 billion is sales in 2013.

The 6 largest global equipment players based on 2014 ag equipment revenue are Deere & Co., CNH Industrial and AGCO, closely followed by Kubota, Claas and Mahindra. In terms of relative size and market share, the report points out that, when it comes to total revenue, Deere and CNH are similar in size. But when only ag sales are considered, Deere’s business segment is 40% larger. Deere is also 2.5 times larger than Kubota and AGCO.

The report authors conclude, “It seems logical that a strategic transaction among this peer group could occur in order to create a more formidable challenger to the market leader.”