The final tally for ag equipment sales is not yet in for the current year, and the larger than usual number of variables dealers and manufacturers are confronting is clouding visibility into 2013.

Each month, Ag Equipment Intelligence and its research partner, Cleveland Research Company, survey farm machinery dealers from across North America to provide ag marketers with a snapshot of dealer sentiments about current business conditions. Subscribers to Ag Equipment Intelligence receive a full report each month — Dealers’ Sentiments Business Conditions Update based on the survey results. The following analysis of 2012 and outlook for 2013 is from Curt Siegmeyer of Cleveland Research Company.

To date, 2012 has been somewhat of a roller coaster ride for the ag equipment dealers and manufacturers. While the year started out strong on the back of strong 2011 cash receipts, we observed a notable level of pessimism from dealers throughout the summer months as many farmers watched the impact of the North American drought drive down their yield expectations.

The result was a pullback on spending particularly on discretionary items and a modest softening in used equipment values as farmers took more of a ‘wait and see’ approach. This, coupled with several consecutive years of strong growth in North America has led to stock prices that have lagged the broader market year-to-date. Thus far, ag equipment sector average is up ~10% vs. 16% for the S & P 500.

The livestock sector is expected to face the most pressure over the next 6-12 months due to higher feed costs, but a silver lining is that we’ve seen a notable change in sentiment and improved demand among North American grain farmers over the last 30-60 days. Farmers have now gained a better understanding of their crop insurance, yields appear to be coming in better-than expected, and many farmers stand to have as good or a better year than initial expectations entering 2012.

In addition, the rally in global crop prices as a result of lower expected supply has boosted the prospects for grain farmers in international markets. This has translated into robust equipment orders and while still early, points to the potential for another record year in 2013 for the machinery companies.

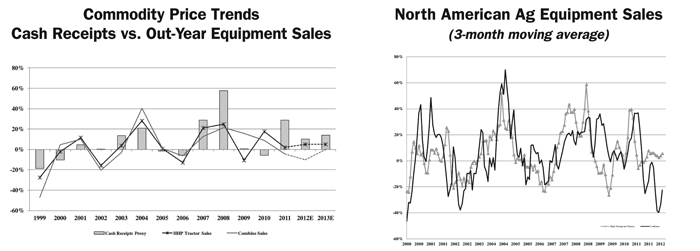

The USDA’s latest (September ‘12) crop supply and demand forecast for the 2012-13 crop year shows a slight negative revision in the Ag Equipment Intelligence-Cleveland Research Company’s simplified cash receipts proxy. The updated projections for the 2012-13 crop year show a modest decrease in our simplified cash receipts proxy as a slight negative price revision in corn and wheat compared to the previous month resulted in lower total cash receipts. Our simplified cash receipts proxy now stands at just over $145 billion, or about 14% above last year’s levels compared to 18% last quarter. Farmer cash receipts are highly correlated with out-year new equipment sales as shown here, so the initial outlook for 2012-13 cash receipts is a cautious indicator for 2013 North America ag machinery demand.