|

According to the national Survey of Terms of Bank Lending to Farmers conducted during the first full week of August, the total volume of non-real estate farm loans was 20% higher than the same period in 2013. Source: Agricultural Finance Databook, Table A.3. |

|

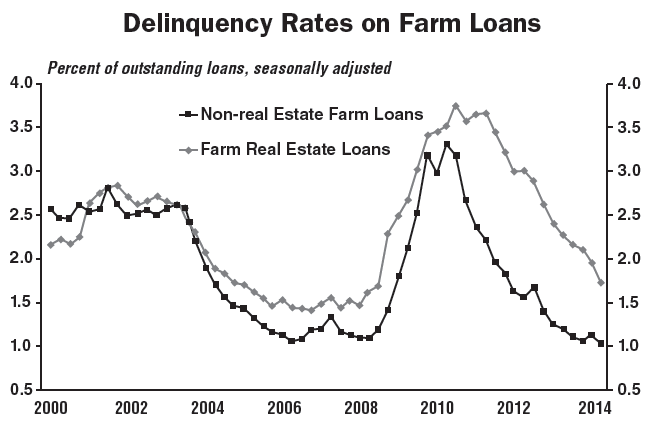

Even with rising loan volumes, delinquency rates on farm real estate and non-real estate loans continued to trend down. Delinquency rates on farm real estate loans dropped the most, from 2.9% to 2.3% of outstanding loans Source: Federal Reserve Board of Governors. |

Short-term financing for ongoing production needs appears to be further restraining medium-term borrowing for capital investments, like equipment and grain storage, according to the third-quarter edition of the Agricultural Finance Databook from the Federal Reserve Bank of Kansas City. The report tracks national trends in farm lending and was authored by Nathan Kauffman, Omaha Branch executive, and Maria Akers, associate economist.

In summarizing the current conditions of farm borrowing, the authors say that “Agricultural lending rose further in the third quarter as commodity price movements continued to increase the need for farm sector financing. Loans to the livestock sector rose alongside sharply higher feeder cattle prices, and operating loans held at high levels as the substantial drop in crop prices over the past year boosted the need for working capital.

“Although debt levels have continued to rise, profitability in the livestock sector, expectations of record yields and revenue support from crop insurance are likely to help lessen the drag on farm income from low crop prices this year. However, depending on the direction of commodity prices and production costs, concerns about lower farm income and rising debt levels could intensify in 2015.”

Spending Spree Slows

As a result, Kauffman and Akers say the “capital spending spree” of the past several years has faded as loan volume for farm machinery and equipment fell during 2014. In addition to the significant commodity price swings in recent years, many farmers took advantage of rising farm income and advantageous tax incentives to upgrade their equipment and to add on-farm crop storage capacity.

As of June 30, 2014, total farm debt outstanding grew by 6.4% year-over-year. The volume of loans secured by farmland and the volume of loans to finance farm production rose at a similar pace, 6.5% and 6.3%, respectively.

Despite the increasing number of loans, farm operators are so far meeting their repayment obligations. “Even with rising loan volumes, delinquency rates on farm real estate and non-real estate loans continued to trend down,” say Kauffman and Akers. “Delinquency rates on farm real estate loans dropped the most at the 100 largest lenders, from 2.9% to 2.3% of outstanding loans, and they also edged down at other commercial banks. Delinquency rates on non-real estate farm loans fell slightly at all commercial banks and reached a historical low of 1%. The charge-off rate for farm loans also fell, except for farm real estate loans at large banks, where they edged higher.”