IN THIS ISSUE OCTOBER 2013

Dealer Business Outlook & Trends Most farm equipment dealers are optimistic about their sales prospects for 2014, but recognize changes are afoot.

In the face of volatile grain prices, uncertainty about depreciation rules, skepticism about a new farm bill and a lot of talk about farm equipment sales peaking, North American farm equipment dealers continue to see good potential for solid sales in 2014. But their optimism is moderating compared to the past two years as each of these factors add an element of indecision for farmers looking to upgrade their ag machinery.

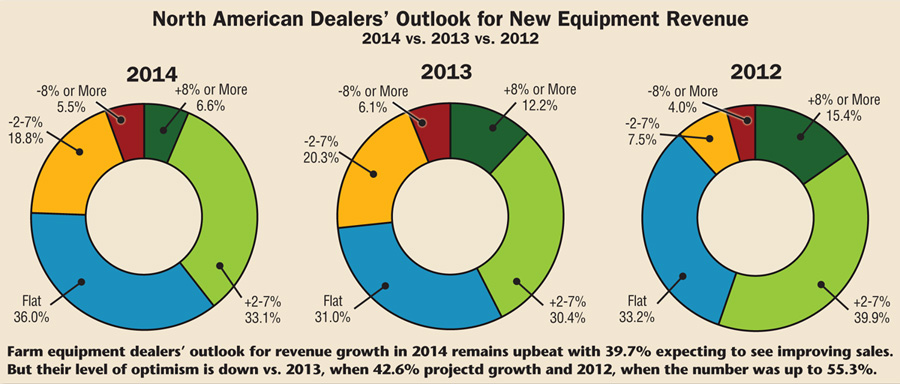

Even with all of these issues hanging fire, nearly 40% of the dealers responding to Farm Equipment’s “2014 Dealer Business Outlook & Trends” survey expect revenues from new equipment sales to increase anywhere from 2% to more than 8% in the year ahead. Another 36% are calling for “flat” sales in 2014. In this case, “flat” sales implies strong business levels as, by all accounts, sales through the first 9 months of 2013 have been stellar.

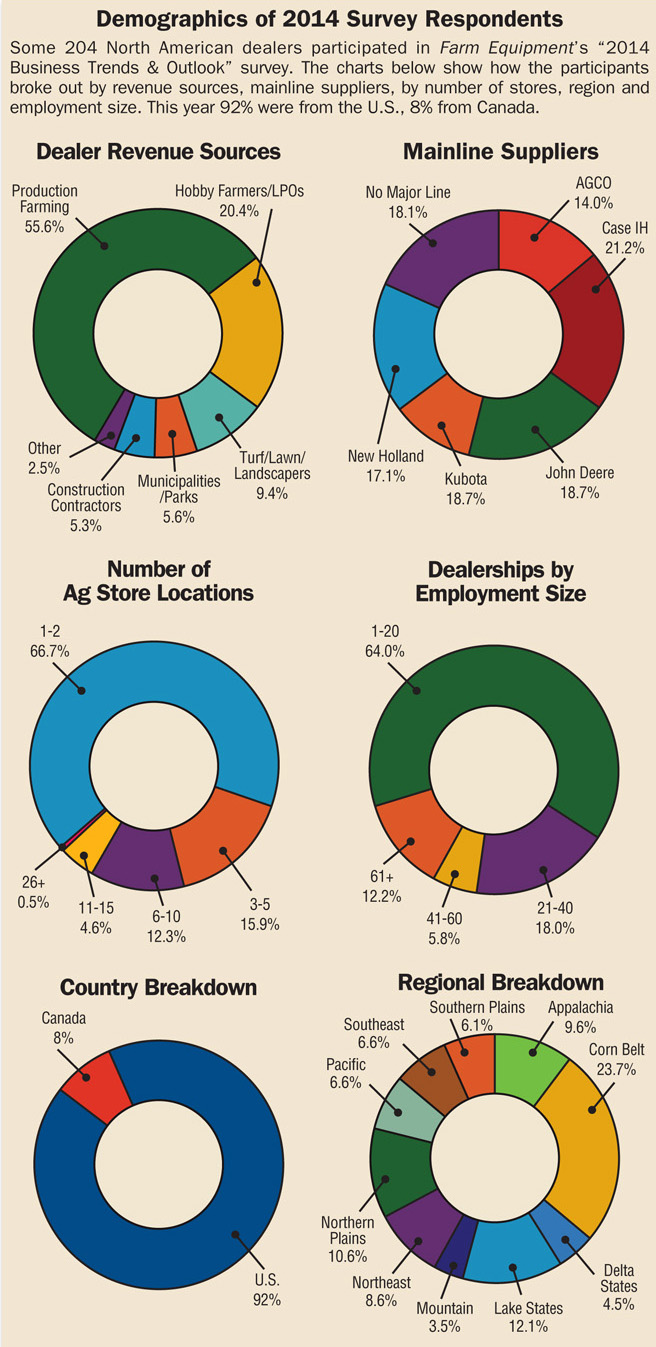

More than 200 dealers from the U.S. and Canada participated in this year’s survey, which was conducted during the last week of August and first two weeks of September.

Sound Farmer Financials

Besides the solid equipment sales seen during this past year, in all likelihood, a good part of the dealers’ confidence is buoyed by the overall financial health of North American farmers. Producers have had a string of strong years that has put them on very sound financial footing.

While this has put farmers in a strong position to be able to invest in upgrading their equipment, they’re also in a situation that could allow them to sit back and not buy as they’ve steadily upgraded their equipment over the past few years.

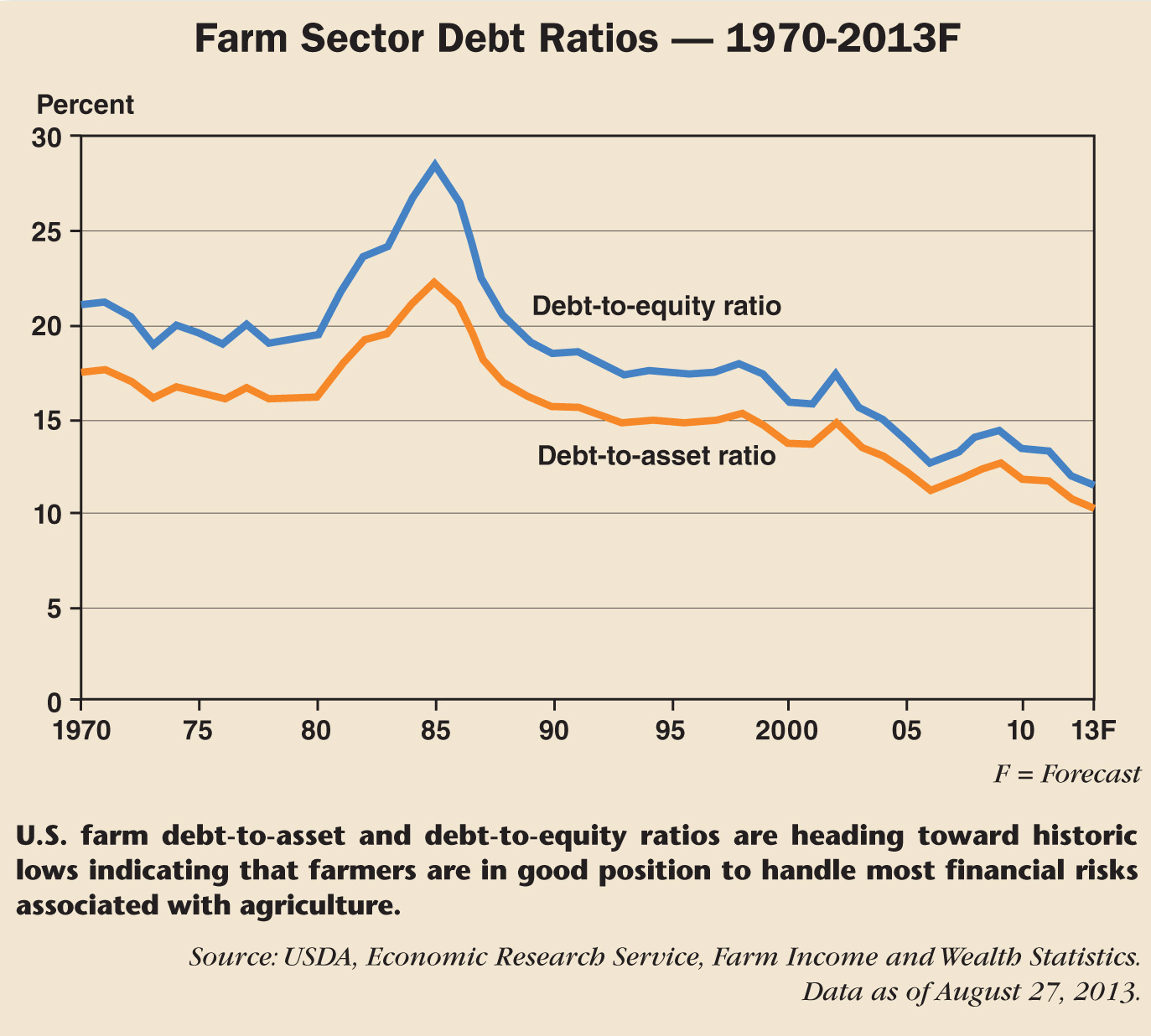

In its “Farm Sector Income & Finances” report released in August, USDA reported that U.S. farms debt-to-asset and debt-to-equity ratios, traditional measurements of farm business sector’s financial solvency, are heading toward historic lows. The ag agency says that, “Based on forecasts of the value of farm business assets and debt, the sector’s debt-to-asset ratio is expected to decline from an estimated 10.7% at the end of 2012 to 10.2% by the end of 2013. The debt-to-equity ratio is expected to decline from 12% in 2012 to 11.4% in 2013.

“If realized, these changes would result in new historic lows for both measures, confirming the strength of the farm sector’s solvency. This strength means the sector is better insulated from the risks associated with commodity production (such as adverse weather), changing macroeconomic conditions in the U.S and world economies and fluctuations in farm asset values,” USDA says.

Of course, the biggest share of the dealers’ positive outlook is based on actual equipment sales, and they’ve held up well through the first 8 months of 2013. Total new tractor sales in the U.S. are up 12.6% January through August according to the Assn. of Equipment Manufacturers compared to the same 8 month period in 2012.

Unit sales of combines also rose by 26.8% through the first 8 months of 2013. Sales of all classes of farm tractors in Canada rose 12.6% during the same period, while combine sales grew 7.8%. But the pace of tractor and combine sales has slowed somewhat in the past few months.

Crop Receipts &

Tractor Capex

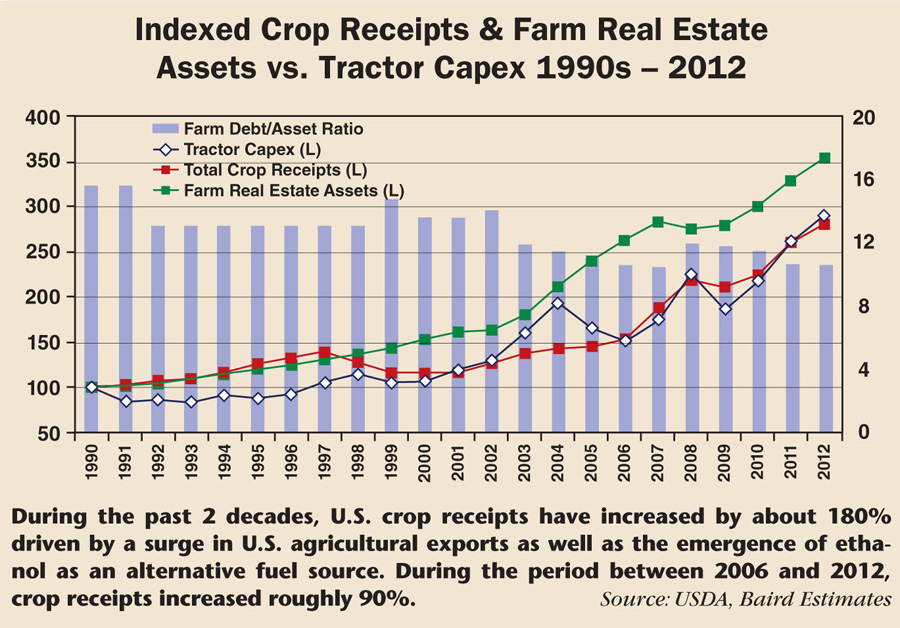

Earlier this year, RW Baird issued a report to investors that underlined how farmers’ capital expenditures in tractors has closely correlated between 1990 and 2012.

According to Baird, during the past 2 decades, U.S. crop receipts have increased by about 180% driven by a surge in U.S. agricultural exports as well as the emergence of ethanol as an alternative fuel source. Increased ethanol production has had a particularly pronounced impact on crop receipts since 2005. During the period between 2006 and 2012, crop receipts have increased roughly 90%.

Prior to this period, from 1970-1980, crop receipts grew 242% while capital expenditures in tractors increased 228%. “Over the subsequent 6 years, crop receipts declined 11% before bottoming out in 1986 while tractor capex declined 59%, also bottoming in 1986,” says the RW Baird report.

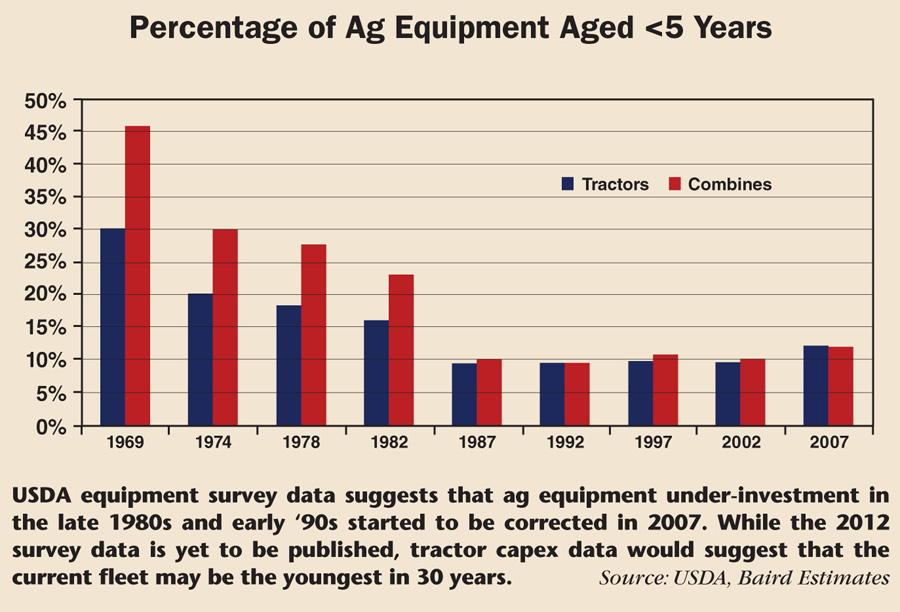

It goes on to say, “USDA equipment survey data suggests that the equipment under-investment experienced in the late 1980s to the early 1990s has started to be corrected as early as 2007 following several years of strong farm capex. While the 2012 survey data is yet to be published, tractor capex data would suggest that the current fleet is meaningfully younger — the youngest in 30 years — given sizable investment over the last 5 years.”

To determine the level of motivation of North American farmers to replace equipment that is 5-plus years old, UBS Investment Research asked the question in its most recent dealer survey in September 2013.

A majority of dealers (76%) reported their customers are “somewhat motivated” — vs. “not motivated” (16%) or “very motivated” (7%) — to replace equipment that is 5-plus years old. Some 30% of dealers reported the level of motivation has declined over the past year. Only 9% said their customers were “more motivated” this year than in the previous year.

A Tempered Optimism

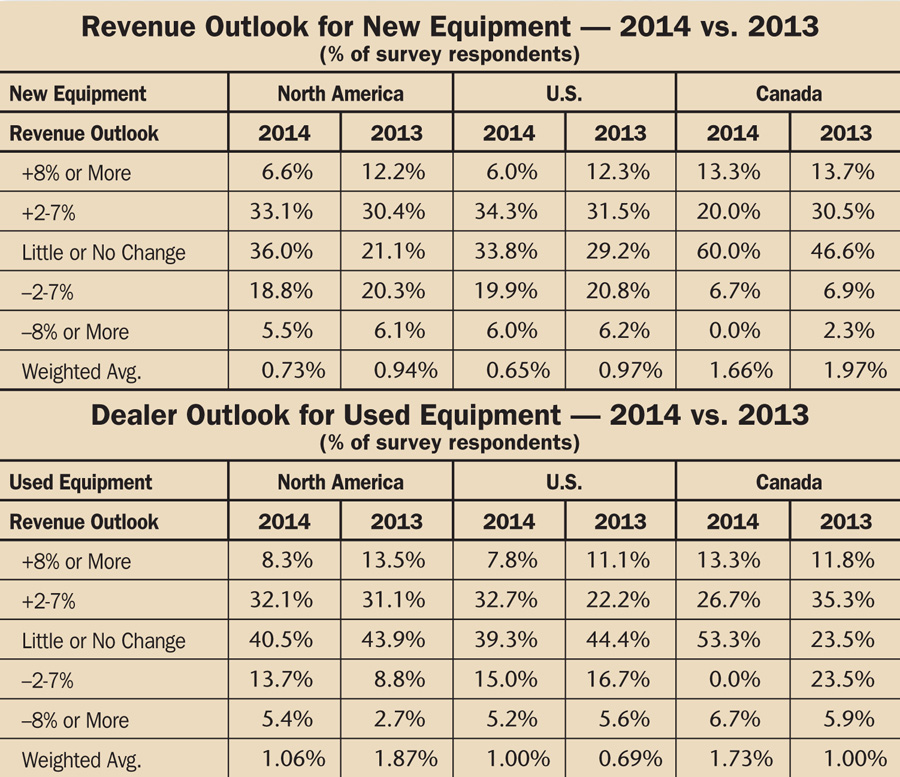

While remaining confident about their prospects for 2014, dealers’ optimism about next year’s prospects are tempered somewhat compared to their outlook a year ago at this time, and even more so vs. 2 years ago. For example, on a weighted basis, the dealers’ outlook for increasing new equipment sales revenues is 0.73%. Last year at this time it was 0.94%. Two years ago, the weighted average of dealers’ responses for new equipment revenues came in at 2.37%.

The biggest shift came in those projecting “+8% or more” growth and in “little or no change.” For the year ahead, there was a 5.6% swing between this year and last for those projecting revenue gains of 8% or more (6.6% in 2014 vs. 12.2% in 2013). Nearly 5% more dealers this year compared with last year are calling for a “flattish” year in terms of overall revenues from the sale of new equipment (“little or no change” 36% for 2014 vs. 31% in 2013).

Otherwise, 39.7% of dealers see sales revenue increasing in the next year compared to 42.6% who fell into that category last year. Actually, fewer dealers are looking for a falloff in revenues for 2014 (24.3%) than there were one year ago (26.4%).

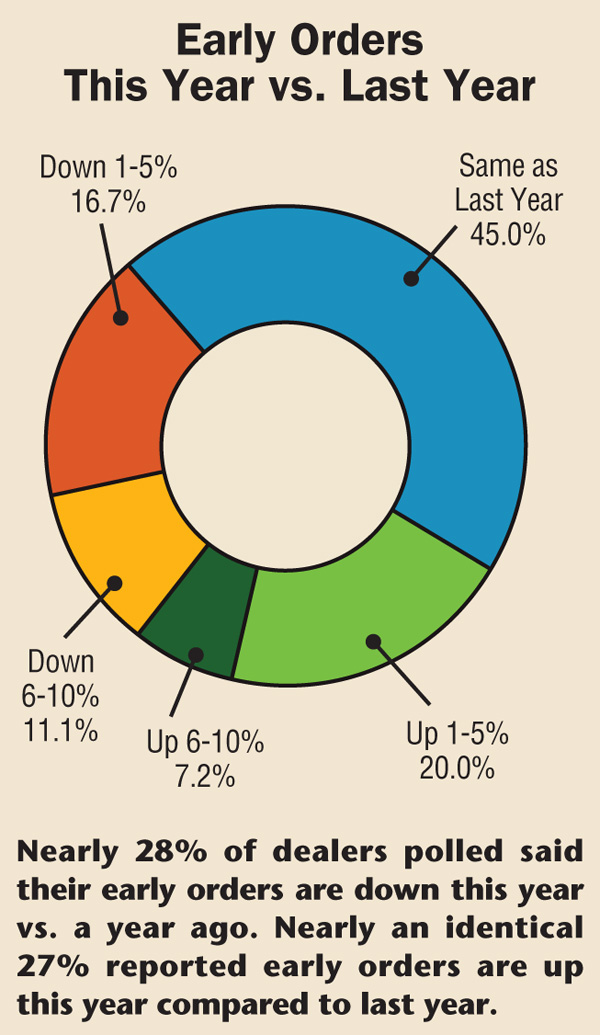

When it comes to early order levels, a nearly identical percentage of dealers (27.8%) say their pre-sells are down this year vs. a year ago, while 27.2% say they’re up. The remaining 45% say early orders are at about the same as last year at this time.

Tractor & Combine Sales

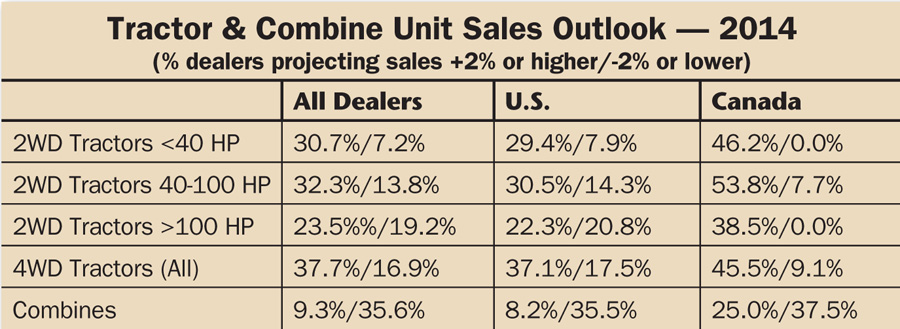

A look at projections for 2014 unit sales for the various categories of tractors and combines, indicates a higher level of optimism for smaller tractors than for the larger models.

As for combines, few dealers are holding out any strong hopes for increasing sales.

The percentage of all dealers expecting higher unit sales of compact tractors (<40 horsepower) in the year ahead increased to 30.7% vs. 27.8% in last year’s survey. Only 7.2% see sales of these units decreasing vs. 13.2% a year ago.

The percentage of dealers expecting to increase sales of mid-range tractors (40-100 horsepower) stayed about the same, with 32.3% projecting higher sales in 2014 vs. 32.1% projecting increases a year ago. The big shift came in the number of dealers looking at declining sales of this tractor category. Only 7.3% project decreasing sales last year compared with 13.8% this year.

The dealers’ view on unit sales for row-crop tractors (100+ horsepower) dipped for the year ahead vs. a year ago. This year, 23.5% of dealers are expecting an increase in sales compared to 29.5% who forecast growth for the tractor class last year. More dealers are projecting a fall off in sales for 2014 (19.2%) vs. for 2013 (11.6%).

The forecast for higher four-wheel drive unit sales in the year ahead also fell back to 37.7% compared to a year ago when 48.9% expected sale growth.

Unit sales of combines took a steep dive in the dealers’ view compared with an already low level a year ago. For 2014, only 9.3% of dealers see the opportunity to increase combine sales vs. 17.2% of dealers who projected growth last year at this time. More than one-third (35.6%) of dealers are expecting sales of combines to decline in 2014. This compares with 21.2% projecting decreases last year.

Pricing Pressures

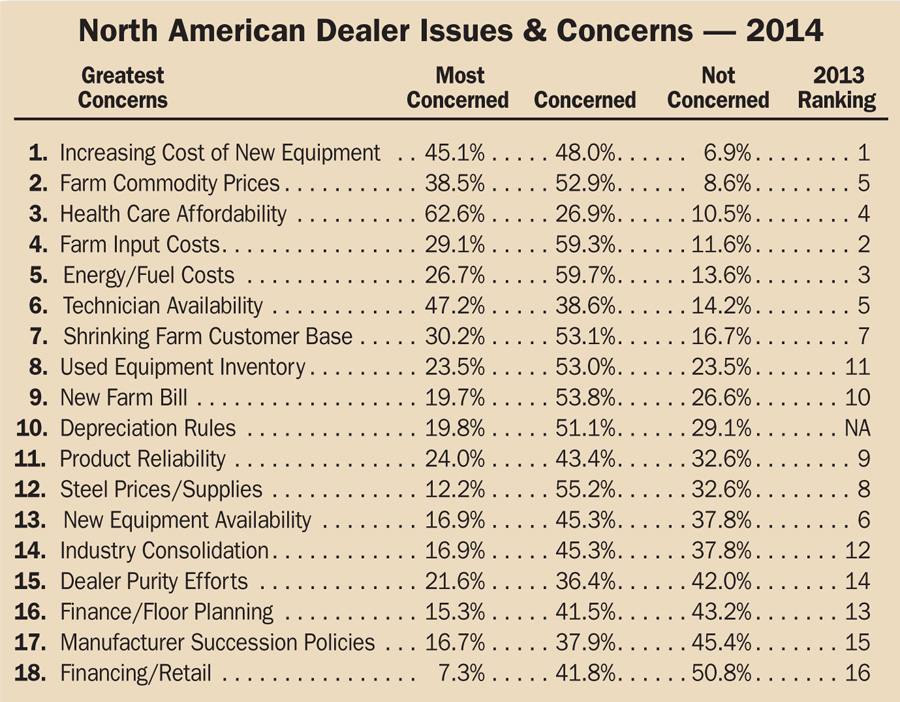

While farm machinery dealers are expressing several significant concerns that could impact new equipment sales in 2014, the one thing that continues to top their list is continually rising cost of new equipment. Like last year, this is the #1 dealer concern going into the new selling season as 93.1% of dealers in this year’s survey indicated that they were “most concerned” (45.1%) or “concerned” (48%) about the increasing cost of new equipment.

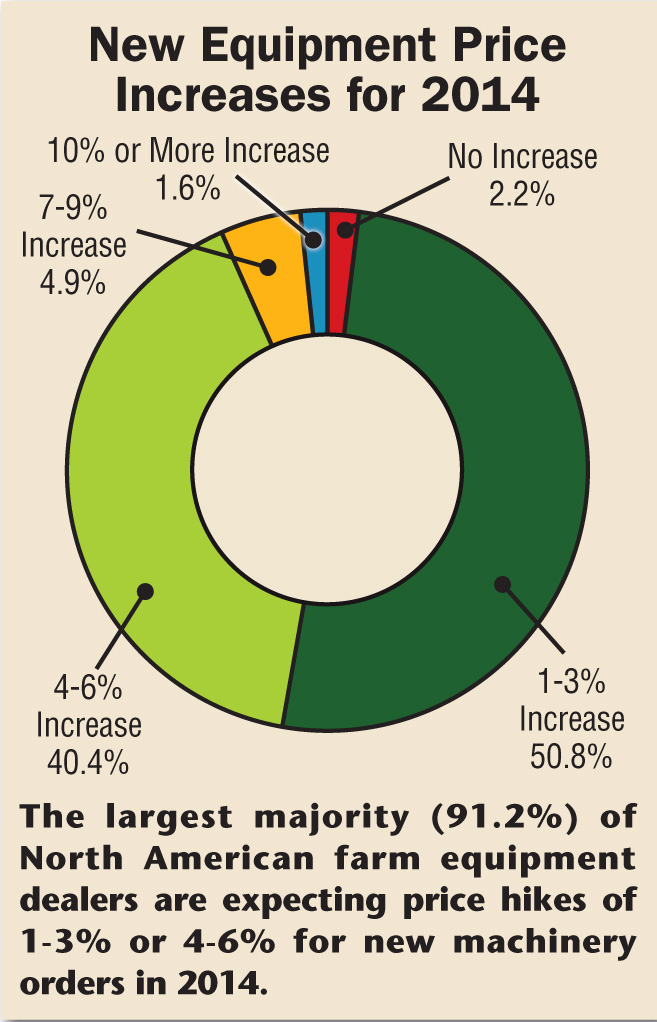

And nearly all dealers are expecting hefty equipment price increases for 2014. Asked if they were expecting the price increase from their mainline supplier, more than half (50.8%) are preparing for a 1-3% hike and 40.4% expect a 4-6% jump in prices.

A smaller percentage of dealers are anticipating higher increases, with 4.9% expecting 7-9% price hikes and 1.6% planning for increases of 10% or more. Only 2.2% of dealers indicated they are not expecting a price hike for new machinery in the year ahead.

Getting a Handle on Used

When it comes to used machinery, dealer sentiments remained generally positive, but concern is evident about its growing backlog. Overall, 40.4% of dealers expect revenues from used machinery sales to increase from 2% to more than 8%. This compares with 44.6% of dealers who expected increases in that same range a year ago.

Last year at this time, 11.5% of dealers projected their sales of used equipment would decline by 2% to more than 8%. That number has grown by nearly 8% to 19.1% of dealers this year who see revenue from used equipment sales declining in 2014.

Noting the difference in dealer views about new equipment revenues compared with used equipment prospects in the year ahead, one Kansas dealer said simply, “New sales will stay the same. I’m much more concerned with used sales.”

Some dealers believe the backlog of used machinery is being exacerbated by their major suppliers push for bigger market shares. As one dealer participating in this year’s survey put it, “Case IH is on our ass to beat John Deere.”

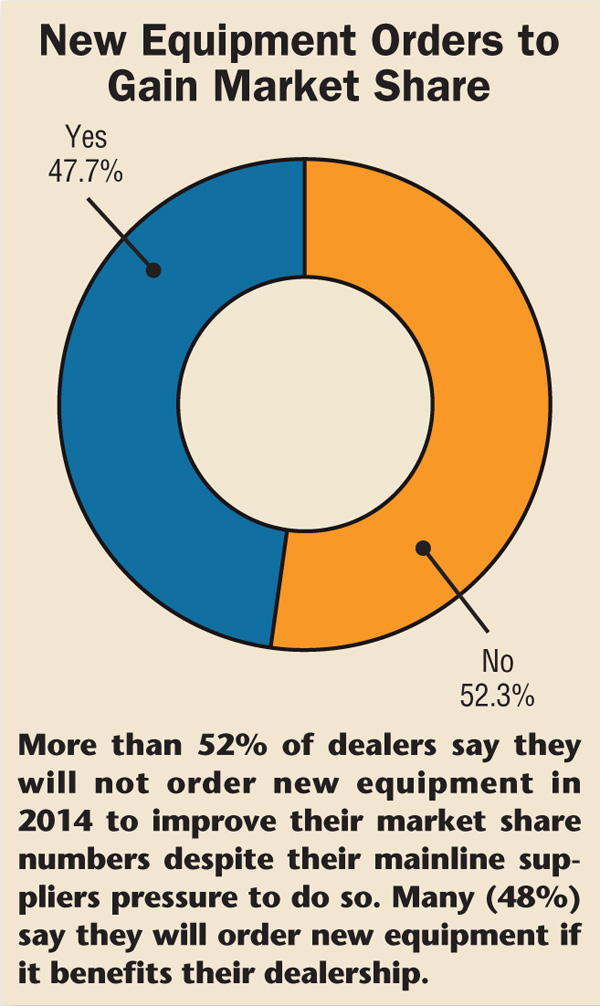

On that subject, in this year’s survey, we posed a new question to dealers: “Considering the push for market share by the major manufacturers, will you continue to place orders for new equipment in 2014 to grow market share even with the glut of used equipment currently in the marketplace?”

It’s clear that dealers are trying, if not succeeding, to resist their suppliers’ pressure to gain market share. Slightly over 52% of dealers responded “no,” they will not continue ordering new equipment to simply to satisfy their suppliers push for greater market share.

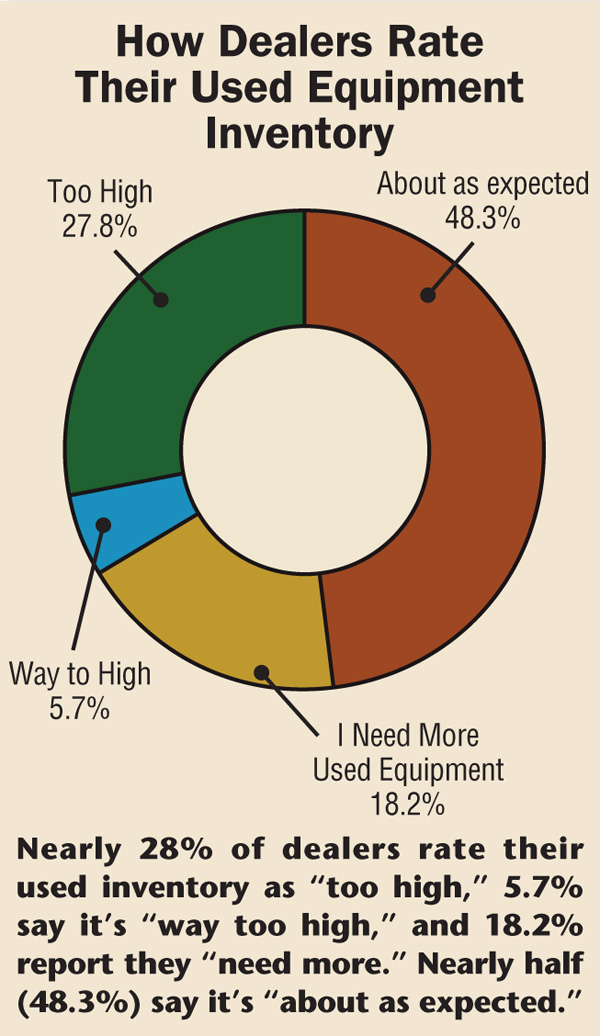

For all the talk about a glut of used farm machinery, apparently most dealers believe their inventories are manageable. Asked to rate their used equipment inventory, nearly half (48.3%) said it’s “about as expected.” Another 18.2% said, “I need more used equipment.”

Only 5.7% indicated their used backlog was “way too high,” while the remaining 27.8% rated their used inventory as “too high.”

U.S. & Canada:

A Similar Path

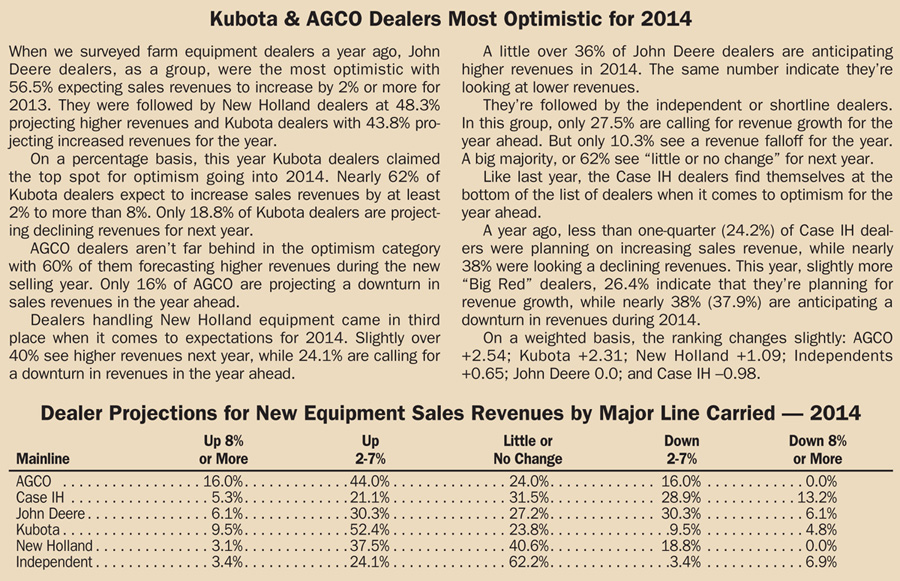

In past surveys, Canadian dealers tended to demonstrate a more optimistic view toward future revenue prospect than their U.S. counterparts. This year, the picture is somewhat muddled, but a similar trend can be observed. On a weighted basis, the trend over the past 3 years demonstrates a remarkable consistency, with the Canadian dealers continuing to show a more optimistic view of the coming year.

The revenue outlook for new equipment from Canada’s dealers registered a 1.66% for 2014 on a weighted basis compared to U.S. dealers’ 0.65% level. A similar spread could be seen in last year’s (2013) survey, though both groups of dealers were somewhat more optimistic: Canada, 1.97% and U.S. dealers, 0.97%. The same trend was seen in the prior year (2012) when both Canadian and U.S. dealers were far more optimistic about the year ahead. The survey results from 2 years ago showed weighted averages of 3.35% for Canadian dealers and 2.24% for U.S. farm equipment dealers.

In terms of straight percentages of dealers looking at new equipment revenue increases or declines for 2014, one-third (33.3%) of Canadian dealers are expecting revenue increases in 2014. This compares with 40.3% of U.S. dealers projecting revenue growth from the sale of new equipment in the year ahead.

Breaking the numbers out by amount of growth or decline is where the biggest difference in dealer views shows up. For Canadian dealers, 13.3% are projecting growth of 8% or more. The percentage of U.S. dealers looking at the same levels of growth came in at 6%. The number of Canadian dealers looking at revenue increases in the range of 2-7% was 20% vs. 34.3% of U.S. dealers.

The major shift in the difference between dealer outlooks for both countries showed up in the “little or no change” or “flat” revenue category. A full 60% of Canadian dealers expect “little or no change” in 2014 revenues from the previous year. Half of that percentage, or 29.2% of U.S. dealers are calling for “little or no change” in new equipment revenues for the coming year.

As for their prospects for declining revenues, only 6.7% of Canadian dealers expect a dropoff in new equipment sales in 2014 and that will come in the range of –2-7%. No Canadian dealers see declines in new equipment revenues of 8% or more.

On the other side of the declining revenues story, 25.9% of U.S. dealers see new equipment revenues falling in 2014. Nearly 20% (19.9%) expect revenues to decrease by 2-7%, while another 6% see a decline of 8% or more.

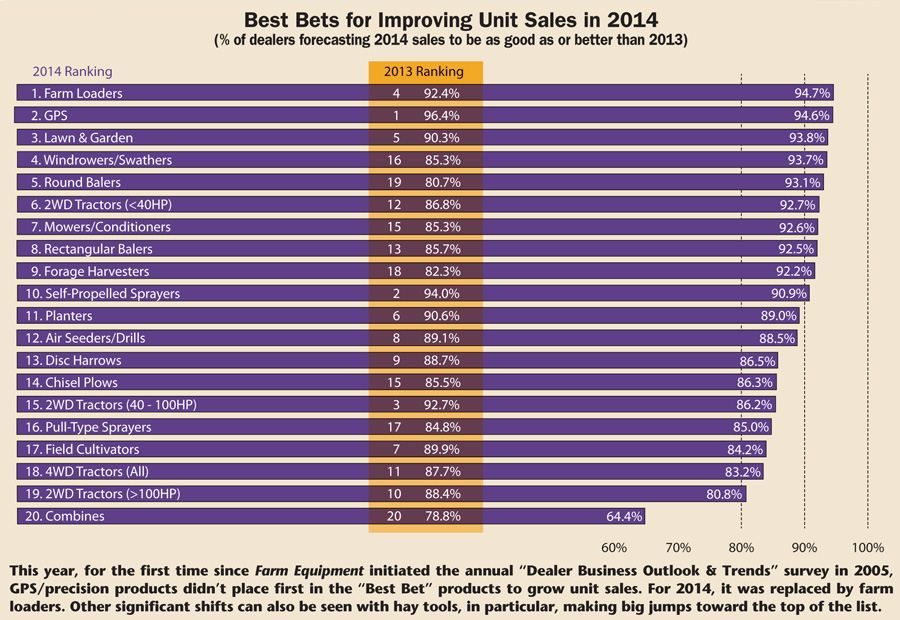

Promising Products for 2014

Based on the percentage of dealers who expect unit volumes of specific equipment to be as good as or better than 2013, farm loaders took the top spot at 94.7%, barely squeaking by the perennial favorite, GPS/precision farming equipment that registered a score of 94.6%.

Farm loaders were #4 on the dealers’ list last year.

Other products in the Top 5 of dealers’ choice for increasing unit sales for 2014 include: lawn and garden products (93.8%), which was ranked #5 for 2013; windrowers/swathers (93.7%) that jumped all the way from the 16th spot last year; and round balers (93.1%), which was second from the bottom, or 19th place, in last year’s survey.

Equipment categories that fell down the list vs. last year’s dealer choices include two-wheel drive tractors (40-100 horsepower) that fell from #3 in 2013 to the #15 spot for 2014. Field cultivators also slipped significantly, from #7 last year to #17 for the year ahead.

When considered on a weighted average basis, the order of “Best Bet” products for 2014 changes somewhat as shown here:

• GPS/Precision Ag +2.37%

• Lawn & Garden +2.24%

• Farm Loaders +1.31%

• 2WD Tractors (<40HP) +1.27%

• 4WD (All) +1.07%

• Planters (All) +1.03%

• Mower/Conditioners +1.00%

• 2WD Tractors (40-100HP) +0.92%

• Round Balers +0.88%

• Air Seeders/Drills +0.56%

• Disc Harrows +0.43%

• Self-Propelled Sprayers +0.39%

• Windrowers/Swathers +0.31%

• 2WD Tractors (>100HP) +0.29%

• Field Cultivators +0.28%

• Rectangular Balers +0.25%

• Forage Harvesters –0.10%

• Chisel Plows –0.28%

• Pull-Type Sprayers –0.44%

• S.P. Combines –1.69%

Vexing Issues for 2014

As was mentioned earlier in this report, the increasing cost of new equipment is the front of mind issue for North American farm equipment dealers. In fact, each of the top 5 major issues for dealers involve either rising or falling prices and rising costs.

Many dealers attribute much of the price increase on new equipment to the new Tier 4 Final engines that equipment makers were mandated by law to develop for the new machines sold in 2014. But higher prices for new farm machinery has been #1 on the dealers’ list for 3 years running, so it isn’t as if it is a new issue. It’s been building for some time. But as long as farmers are making more money than they have in decades, it will probably remain tolerable for the time being.

Based on our method of scoring — most concerned + concerned — in second place behind rising new equipment prices are concerns about falling commodity prices, which was ranked #6 on the dealers’ list of concerns last year. In this most recent survey, 38.5% checked “most concerned” and 52.9% checked “concerned” in regard to the urgency they feel toward the current lower commodity prices.

As of September 15, December futures for corn ended the week at $4.56 per bushel and wheat ended the week at $6.41. November futures for soybeans ended the week at $13.48 per bushel. Year-over-year corn prices were down 35.5%, soybeans down 14.4%, and wheat down 27.2%.

Also, it wasn’t unexpected that health care affordability would be near the top of dealers’ biggest concerns going into 2014. In fact, if we had only considered the rating of “most concerned” in our rankings, it would have been #1 with 62.6% of dealers listing it as their biggest concern. Another 26.9% checked “concerned,” for a combined total of 89.5% of all respondents. With or without the Affordable Care Act, affordable health insurance has perennially been a Top 5 issue for dealers and little change is expected for the foreseeable future.

Farm input costs followed at #4 with 88.4% of dealers indicating they were “most concerned” (29.1%) or “concerned” (59.3%). Energy and fuel costs rounded out the dealers 5 top issues in the year ahead with 86.4% of dealers indicating “most concerned” (26.7%) or “concerned” (59.7%).

The availability of service technicians has also been an urgent concern of farm equipment dealers. This year it placed sixth on their list. Now, with the push for talented techs who are knowledgeable about the new precision farming equipment and systems hitting the market, this is an issue that promises to only get worse.

The continuing consolidation of farms into bigger and bigger operations, medium-size farmers are becoming a disappearing breed. Rated as dealers’ #7 biggest concern, farm equipment retailers can empathize with those farmers who are being forced to get bigger or get out.

The biggest shift in dealer concerns came with new equipment availability, which came in at #14. Last year, dealers had it at #7 on their list and at #5 the year before. Either new machinery is more accessible or dealers have adapted to its lower levels.

Dealer Spending to Decline

One might think that following several strong years of retail sales, dealers may be inclined to increase their investment in equipment and facilities, but that doesn’t appear to be the case for 2014.

It may be a case of dealers have already spent to upgrade their facilities over the past few years and don’t have the need to do so in the year ahead. Or possibly, with so many good years behind them, they’ll start putting money away for the eventuality that business could slow down.

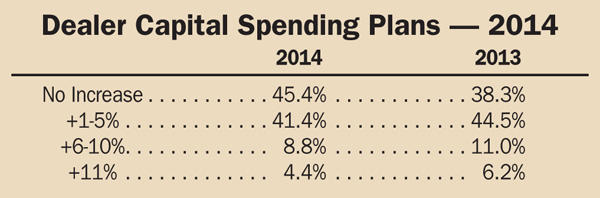

In any case, when we asked dealers about their capital spending plans for next year, 45.4% indicated they will not increase investments in capital expenditures in 2014. This compares with 38.3% who, last year at this time, said they were not planning to increase their investments.

Slightly over 40% of dealers do intend to increase their spending in the year ahead by 1-5% vs. 44.5% who planned to invest in that range last year.

Less than 9% plan to increase their capital expenditures by 6-10% in 2014. This compares with 11% who fell into this category a year ago. The remaining 4.4% say they’ll increase capital expenditures by 11% or more. This compares with 6.2% last who said they intended to increase capital spending by this amount.

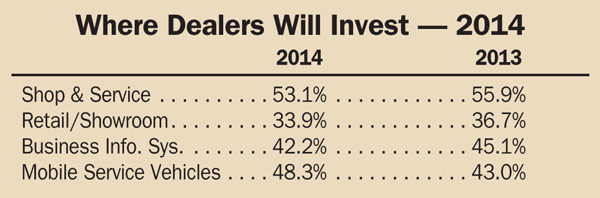

As for where dealers intend to make their biggest capital investments, as usual, the top spot went to their shop and service areas. More than half (53.1%) plan to increase spending to enhance these areas. This is down only slightly from last year when 55.9% said they would increase capital expenditures to improve their service and shop operations.

Not surprisingly, mobile service vehicles are next on the dealers’ list of capital spending. Nearly half (48.3%) say they’re planning to increase spending on service trucks. This compares with 43% of dealers who indicated they were planning to up their investment on mobile service vehicles last year.

Business information systems are next on dealers’ list of spending for 2014. Slightly more than 42% of dealers expect to invest in upgrading their systems vs. 45.1% who said they would do so last year.

A little over one-third (33.9%)of dealerships will invest in the retail operations and showroom areas of their stores in the year ahead. This compares with 36.7% who said they would do so last year.

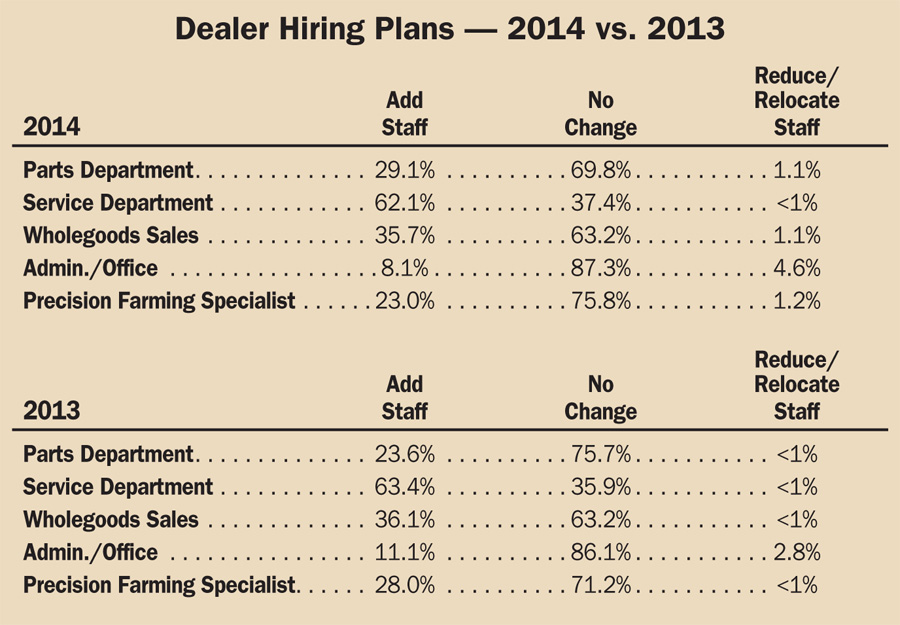

Techs Top List

of Personnel Needs

In this year’s Farm Equipment survey, as has been the case every year, service technicians remain at the top of dealers’ want list when it comes to increasing staff in 2014.

Dealer Commentary on the Push for Market Share Considering the push for market share by the major manufacturers, will you continue to place orders for new equipment in 2014 to grow market share even with the glut of used equipment currently in the market place?

“We hope AGCO will buy market share.” … “There’s only so much your dealership can handle, stay within your capabilities and make yourself a good honest markup!” … “Now that our bonus structure includes market share, it becomes a large part of our take home pay!” … “We are working to reduce used equipment and will continue to push for market share.” … “They cannot keep shoving equipment down to dealers and then take away floorplan terms.” … “Buying the market is not a good long term business plan!!!” … “Customer demand will require it. We’ll ask for greater cash difference and expect to get it.” … “Case IH is on our ass to beat John Deere.” … “Companies are forcing it on to dealers.” … “As long as the order programs are good.” … “Our orders will match need, but we do recognize the need to keep our fair share of new product in the mix.” … “If I can’t make money on it, I am not selling it!” … “I’ll take my chances with market share and would rather make profitable deals.” … “I will order what I think will move and not be intimidated by the company’s market share.” … “John Deere does not let us over order — preset inventory levels.” … “Manufacturers push inventory on dealers knowing we’ll sell at cost if we have to.” … “We need to make money first, and we aren’t going to send used pieces to auction at a loss to achieve market share on new pieces.” … “We have to in order to have iron in the pipeline.” … “We order what we need to stock plus a little to keep our suppliers happy.” … “New is causing the used problem so there is really only one answer: cut new sales and increase prices on new sales.” … “While market penetration is important, sound business decisions must not be sacrificed in favor of market share subsidies.”... “If we can’t reduce our used inventory, we will reduce our new orders. We understand that this may be a bitter pill, but if we can’t sell the used, we can no longer sell the new and the best way to prevent that is to not order the new in the first place.”

Nearly two-thirds (62.1%) of North American dealers say they intend to add more service techs to their employment rolls, if they can find them. As pointed out earlier, 86% of dealers say they are “concerned” or “most concerned” with the availability of technicians to work in their shops.

As the technology of Tier 4 engines and the level of increasingly sophisticated electronics on farm machinery continues to emerge, the urgent requirement for talented technicians will continue to grow exponentially for the foreseeable future.

More than one-third (35.7%) of dealers also plan to add to their wholegoods sales staff for 2014.

This is nearly an identical percentage (36.1%) from last year indicating that the need for qualified salespeople is not diminishing.

What might be most interesting in this area is the increased demand for parts counter people.

Last year, 23.6% of dealers said they were looking into hiring people for their parts department. This year the percentage of dealers looking for parts staff jumped to nearly 30%, which would seem to indicate that the parts business of equipment dealerships is expanding. Some dealers have also indicated that they are starting to lose veteran parts staffers to retirement and are finding it more than a little difficult replacing them.

Two years ago we added the title of precision farming specialist to our list of positions that dealers need to fill. The first year, 19.9% of dealers said they were looking for talent for their growing precision business.

Last year, the percentage of dealers looking for precision specialists jumped to 28%. So it was a bit of a surprise when the percentage of dealers looking for staff for the precision farming departments actually fell by 5% to 23% of dealers looking to fill those slots.

The demand for administrative and office staff also slipped this year. Only 8.1% of dealers say they will add personnel for their administrative operations in the year ahead. This compares with 11.1% who said they were planning to do so last year at this time.

Crop Prices &

Dealers’ 2014 Outlook

As an open-ended, follow-up question at the end of our “2014 Dealer Business Outlook & Trends” survey, we asked dealers, “With the crop prices hovering where they currently are, how does it affect your outlook for 2014 sales?”

Of the 204 total responses to this year’s survey, 140 dealers offered their comments. Here’s a sampling of their commentary and the common threads that ran through them.

Still Positive. “Still optimistic.” … “Cautiously optimistic.” … “Could look good for dairy.” … “Very positive … Record gross farm receipts.” … “2014 sales projections still positive.” … “Still feel that 2014 will be strong — flat to 10% growth.” … “Stable to up 1-5%.” … “Most customers are more optimistic about purchases.”

Cautious & Hopeful. “We will be cautious in ordering new equipment.” … “Hope cattle prices hold.” … “Not good, but I think corn prices will come up.” … “The corn is not in the barn yet.” … “It will depend on yield. However, lower row-crop prices will pave the way for the livestock producer to make a profit. Look for lower numbers in row-crop equipment.”

Could Be a Tough Year. “Down 5-10%.” … “Negative.” … “Slight decrease.” … “Causing concern.” … “My outlook has gone from neutral to negative.” … “Not looking good at all.” … “Crop prices combined with lesser yield in 2013 will negatively impact our 2014 equipment sales.” … “Crop prices are dropping and so are equipment sales.” … “Retail sales will follow crop prices down.”

Pragmatic. “From what I see, there will be higher prices causing less grain to be stored and more being sold off the combine. With this being said, I am going to forecast a big push at the end of the year and 2014 will start off at a slow pace.” … “Hey, it’s all about the farmer having revenue. He’ll spend it if he has it!”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}