As we move into the summer of 2026, the combine market is in a better place than it was a year ago. Not dramatically better, but measurably. For dealer principals and used equipment managers who have been grinding through a difficult inventory correction the last few years, that distinction matters.

Class 8 combine supply is down 16% year-over-year, and it sits 37% below the peak we saw in August 2024. That is real progress. The inventory problem that defined 2024 has not gone away, but it has shrunk. If your dealership has been disciplined about moving equipment, you are likely enjoying a better position heading into this harvest season than you were heading into last year.

The inventory that remains, though, tells a story worth paying attention to. Roughly 63% of all Class 8 combines currently on dealer lots are under 1,000 separator hours. That is a heavy concentration of late-model, low-hour machines. The good news is that it was 66% a year ago, and average hours in this segment have climbed, so the mix is improving. The concern is that it is still concentrated at the high end of the value spectrum, which creates a washout bottle neck risk heading into a selling season where buyer demand, and their liquidity is not as high as we would all like it to be.

Signals in the Market Values

On the retail side, average dealer advertised prices have fluctuated this past year depending on dealerships’ inventory mix and seasonality. Average values for low-hour, late model machines are down just slightly year-over-year.

The auction market provided some signals in the tea leaves this spring, but harvest equipment at spring auctions are generally weak, and those auction signals were there, but diluted as expected. Just as we saw in 2025, there were very few of these machines hitting the block in spring 2026, when compared to 2024. Having said that, average values for low-hour Class 8’s in the 250-1,500 machine hour range were down about 9% year-over-year. This is telling me that there are enough options out there that buyers aren’t going to chase machines that don’t exactly fit their operation’s needs.

There are more promising signs on the higher-hour side. In the 1,500-3,500 machine hour category, values ticked up almost 5% at auction year-over-year. This is especially promising considering that actual sold retail values for that same range increased meaningfully. These actual sold values are the part of the market generating the most promising data points right now, and it is worth having access to.

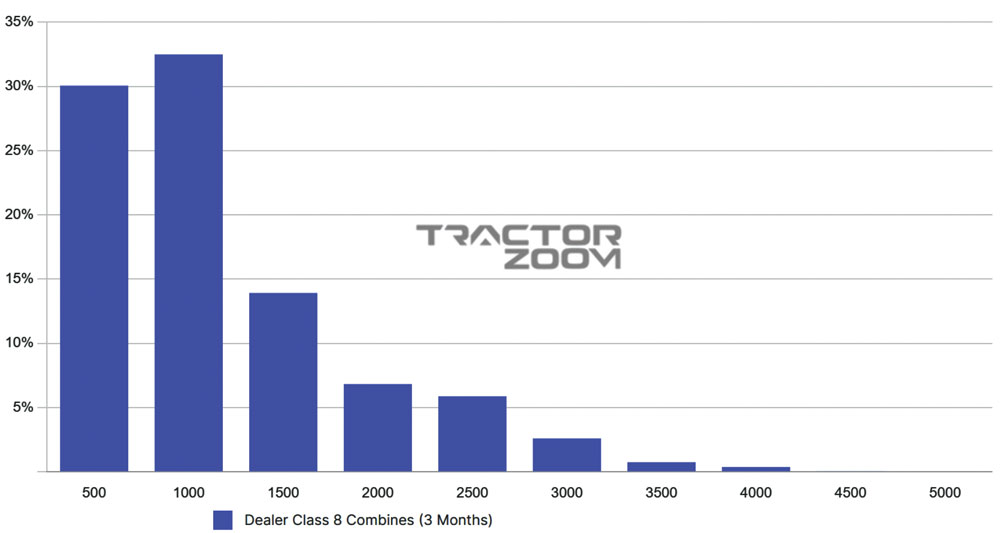

Class 8 Combines Listed by Seperator Hours Range. 100 total units. Tractor Zoom Pro

Lately, I’ve been spending a lot of time looking into the changing “deltas” or differences in values as compared to actual sold values. The delta between retail list and sold, ran 10% on average in the second quarter of 2025, and has tightened to 6.5% in the second quarter of 2026. That is a meaningful improvement, telling me that sellers and buyers are finding each other closer to a common number than they were a year ago. That is important considering the other, more unpredictable, input cost hikes farmers are dealing with this year.

When you look at specific models, the data is even more interesting. Actual sold values for late-model John Deere S780s and Case IH 8250s, specifically those under 1,200 machine hours, are running well above recent trend lines over the last 30 days. Buyers are chasing machines with life left in them, and they are paying for it. The chart below compares S780 auction sales, dealer list prices, and actual sold values from late March through late June. It is rare to see the average of a substantial number of actual sold exceed dealer list value, but it did happen this spring.

A Major Data Gap & Why It Matters

Here is where I want everyone to sit in contemplation for a minute.

If your team is not paying attention to any market data this year, you’re flying blind in a changing storm. Auction volume this year is lower than average. That means fewer publicly visible data points. If your team is leaning on auction comps as the primary source of truth for where the market is, you have some visibility, but are working off a thinner and potentially more distorted data set than you realize. List prices will give you a directional read, but they lag the market and can be distorted based on other dealers’ pricing practices. They tell you where sellers hoped to be, not where deals actually got done.

Sold S780 data for Q2 2026. Tractor Zoom Pro

What will be really valuable this summer, are real-time sold transaction data from the dealer channel. The price points where actual buyers and actual sellers are meeting right now. Tractor Zoom Pro sources those reported sold values directly from dealers in exchange for access to the same data network, and in a low-volume auction environment, that kind of transparency is not a nice-to-have. It is the difference between pricing to the market and pricing to a ghost.

Why Certain Markets are Shifting

Like planting a tree, the best time to address an inventory problem was years ago. The second best time is now.

If you are carrying units that have a real probability of moving this selling season, lean into that. The data supports optimism for certain machines at the right price. But if you are holding combines, or other machine categories that have low odds of retail this summer, hope is not a strategy. Look at where auction values are closest to current actual sold data, and start thinking about what it actually costs you to carry that unit another 90 days versus what it costs to move it at auction today. Some of the dealerships we are working with who are having the best success this year are the ones who made tough inventory decisions two years ago, and now their market demand is rebounding as a result.

The auction market for combines is not flooded right now, and likely won’t be this summer. That matters a lot! Units sent to auction in a thin-supply environment often perform better than the baseline average, especially if the machine is decent quality. A potential buyer who isn’t already in your CRM’s pipeline may never materialize, and that wait has a real price tag.

If you don’t already have it, ensure you have access to actual sold data. Then you’ll see the signs where markets are gradually improving. Then take advantage of those areas with a plan, not a wish.

Trade Values & Trends is brought to you by Tractor Zoom.

Tractor Zoom transforms and connects big data into real-time actionable insights, accelerating a dealership’s heavy machinery and farm equipment business. Our solution, the only one providing transparent, comparable sales data, connects multiple data systems into one easy to use CRM and equipment valuation platform, empowering dealers to optimize decisions, maximize inventory turns, and increase your team’s efficiency and effectiveness. Spend less time on unproductive tasks and more time growing your customer base as we revolutionize the way you drive profitable decisions in the equipment industry.

Andy Campbell is the Director of Insights at Tractor Zoom, where he helps equipment dealerships turn data into faster decisions, better alignment, and stronger margins. Raised on a multi-generation Iowa farm, Andy blends deep ag roots with experience in Fortune 500 companies, tech startups, academia, and as a consultant to make sense of what’s really driving the farm equipment market.