The farm equipment industry is changing rapidly on a number of levels. Recognizing the changes and being prepared to tackle them are paramount to succeeding as a farm equipment dealer. George Russell, an executive partner with Currie Management, presented the keynote speech — “The Changing Structure of the Farm Equipment Dealership” — during the inaugural Dealership Minds Summit touching on how and why the industry is transforming the way it does business.

“There is a lot of change going on in our industry; a lot of change that affects dealerships. But the bottom line is really about how we absorp and act on the data that identifies industry trends,” Russell says.

Pulling from both his personal and profession experience, Russell’s presentation touched on three main themes: people, technology and the drivers of business change. What it boils down to, he says, is it’s people are really at the center of everything that makes your business a success.

Drivers of Change

The questions that every dealer is asking are: “How do we make money?” and “How do we sustain our businesses for the long term?”

Russell says to answer these questions, dealers must recognize the five major changes or drivers that are changing the way dealers do business: consolidation, globalization, technology, resources and regulations and politics. And the first question dealers should ask is, “What are our customers going through,” he says. By answering these questions, it will answer dealers’ questions about making money and remaining sustainable.

For example, all dealers sell very productive equipment. “If a farmer wants to increase his productivity, he can trade in a 300 horsepower four-wheel drive tractor and get a 600 horsepower tractor. He can then put a bigger implement behind it and he’s significantly improved his productivity,” Russell says.

“Now that you’ve helped the farmer increase his productivity, what are you doing in your dealership to match his increased productivity? Improving productivity in a dealership isn’t as easy as simply adding more horsepower,” Russell says. The changes dealers need to make are more incremental.

“You can’t go double what a parts person can sell per year, and you can’t take a technician that you pay 2,000 hours a year and have him double his productivity.

“That’s the fundamental question that is driving what is happening with your end users. They demand more from what they ask from you.

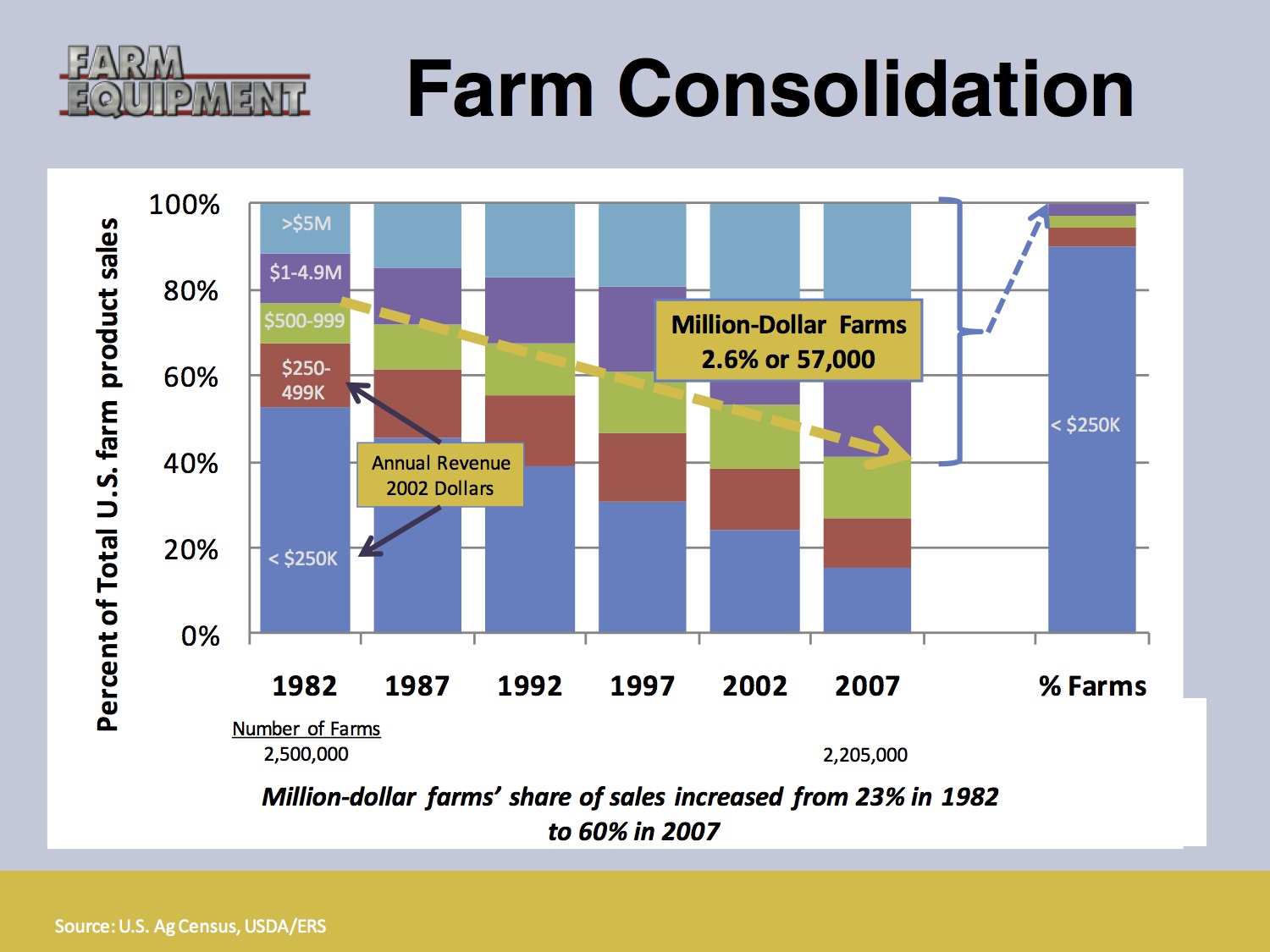

Industry Consolidation

The most obvious driver in the farm equipment business today is consolidation. This is what’s driving this industry in a new direction, and it starts with farm consoldiation.

In 1982, 23% of the farm income was generated by farms that sold a million dollars or more. This has grown and today, adjusted for inflation, million dollar farmers account for 60% of all income. And the number of farms that produce 60% of all the business is relatively few, only about 57,000, according to Russell.

To illustrate this point, Russell explains that 60% of all the business comes from the number of farms that would fit into Lucas Stadium in Indianapolis where last year’s Superbowl was played. Comparatively, farms that produce the remaining 40% of the business encompasses the population of Houston, Texas.

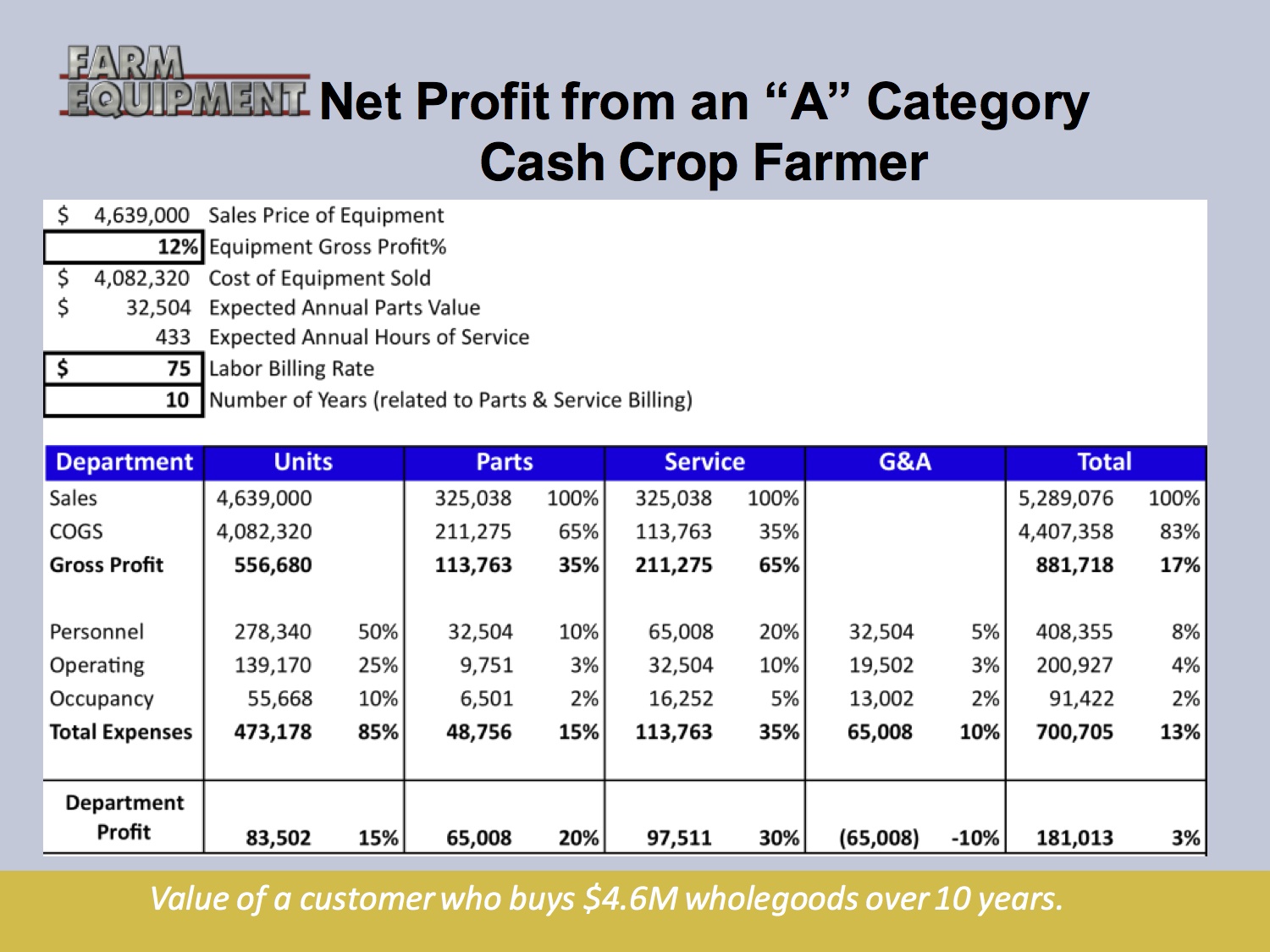

“You have to sell to both of these customer bases,” says Russell. “You have to sell to the big guys, the “A” category farmers, but your second and third trades and parts and service business must come from the smaller “B,” “C” and “D” farmers. So you’ve got challenge in terms of how to sell to both, and you can’t afford to ignore any of these customers.”

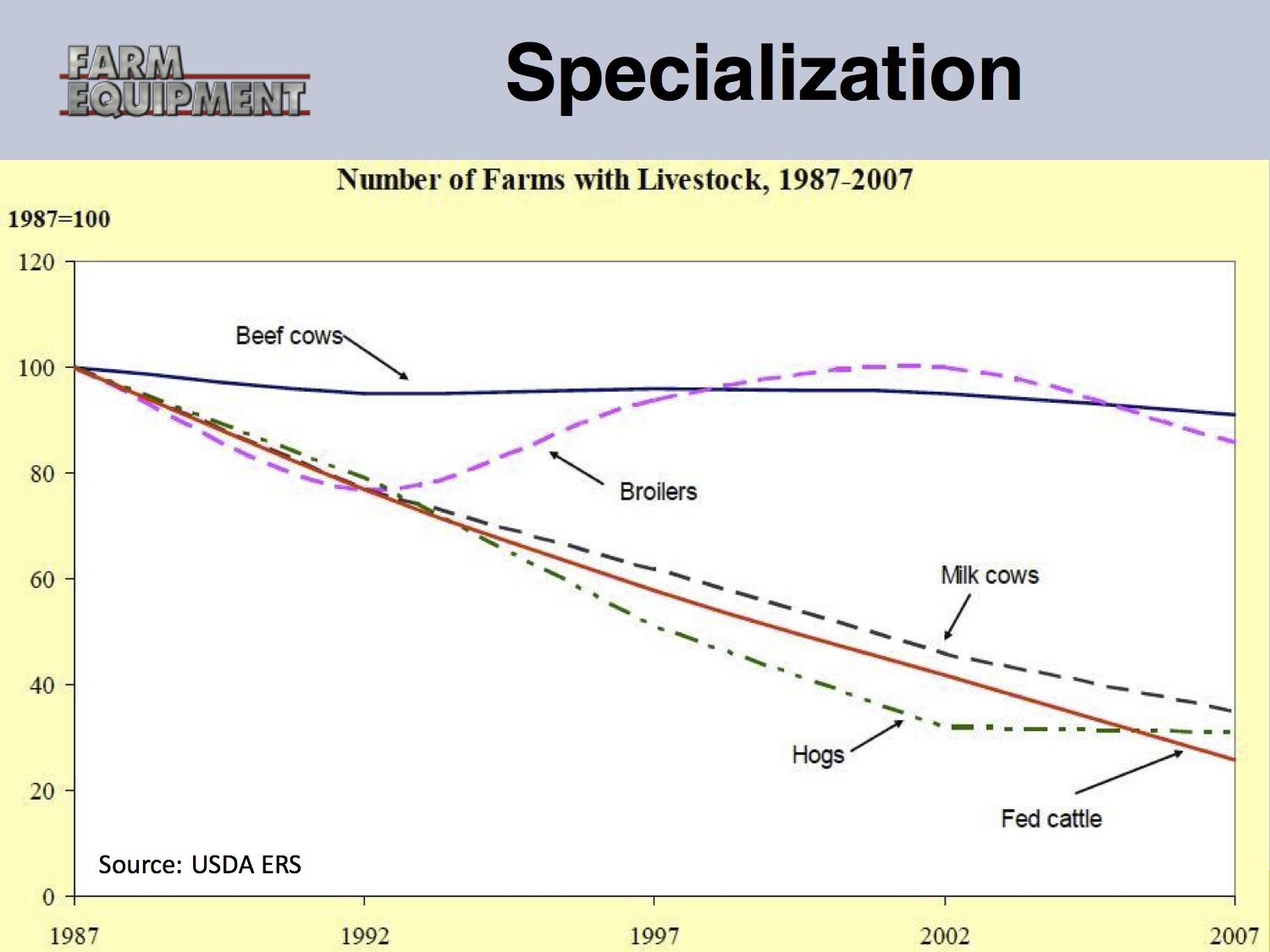

And then, he says, dealers must also deal with more and more specialized farming operations. “You can see the number of livestock operations has dropped significantly. As farms get more specialized, the dealer’s business is getting more specialized, too.”

Russell also points to dairies where there have been major shifts as these operations have relocated to more business friendly regions of the country. “This specialization has changed the nature of the business for a lot of dealerships.”

Dealer Consolidation

The point is that as farms have consolidated and gotten bigger, dealers have had to follow their lead.

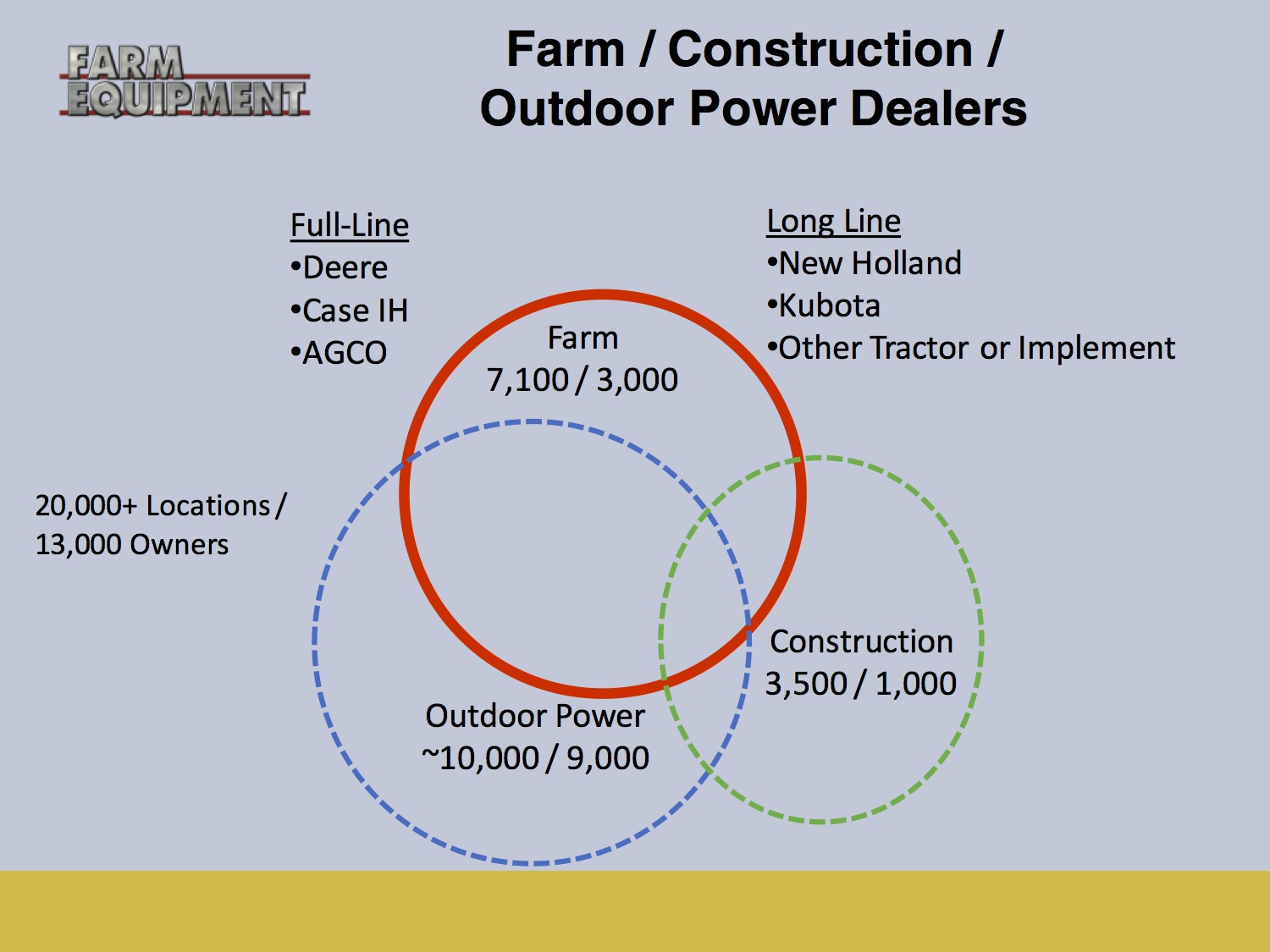

According to Russell, when you take a look at the numbers of farm equipment, construction and outdoor power equipment dealers, there are about 20,000 locations with 13,000 owners. Of those, he says, farm equipment dealers make up 7,000 locations and 4,600 owners. Russell broke these down into type, size and brand to give a clearer picture of what today’s industry looks like.

When classifying dealers by type, Russell explains that at one end of the bell curve you see the publicly traded companies. This is a pretty exclusive club with only three dealership groups with 110 farm equipment locations. (These numbers only represent their ag locations and do not count total locations, which may include trucks, construction equipment and/or industrial equipment like lift forks, etc.)

Next is a group of large private companies, many of which are a single brand, some of which have multiple brands including Case IH and New Holland, AGCO/Kubota, Deere/Kubota, and then there are some dealers that sell machinery and products into multiple industries like construction equipment, trucks, lift trucks, fertilizer.

The next group are what Russell calls “emerging consolidators.” These, he explains, “are dealers who have the ambitious skilled managers. They are true entrepreneurs who make our business so exciting to be a part of and have a clear vision for the future. They don’t always know how they’re going to get there, but they’re putting their fortunes online to try to grow a business and are looking to the future. They tend to be a bit smaller, but their vision is firmly focused on growing, either organically in their current locations or by adding locations.”

Following the “emerging consolidators” on Russell’s list are those he terms “viable” dealers. “Many of these types of dealers operate one or two stores, and many run a good business that put good money on the bottom line. These dealers are very much about expense control and attention to the customer, and have a future,” says Russell. “The biggest question for this group is what is their succession plan?”

And then there is a large group of locations that are either “small and struggling” or clearly “struggling,” according to Russell. “These represent the other end of the spectrum. We see larger dealers who aren’t putting enough on the bottom line; who don’t have sustainable businesses. They need to do some things differently if they’re going to succeed. There are quite a few of dealers in this group. For dealer groups interested in expanding, these dealers may be candidates for acquisition.

But regardless if a dealer or dealer group is buying or selling, whether they need the capital to grow or are making themselves attractive to be acquired, they must improve their financials, says Russell. “There are still a lot of these in the industry.”

And then there are some manufacturers who have chosen to go direct for different reasons. According to Russell, Claas is doing this in Nebraska; Haggie goes direct with sprayers; and Krone has introduced company stores for their self-propelled forage harvester in Wisconsin and California out of necessity.

“Company stores by and large have not succeeded because manufacturers and dealers are like Mars and Venus,” Russell explains. The retail side of the business is just not their forte.

Dealers by Brand

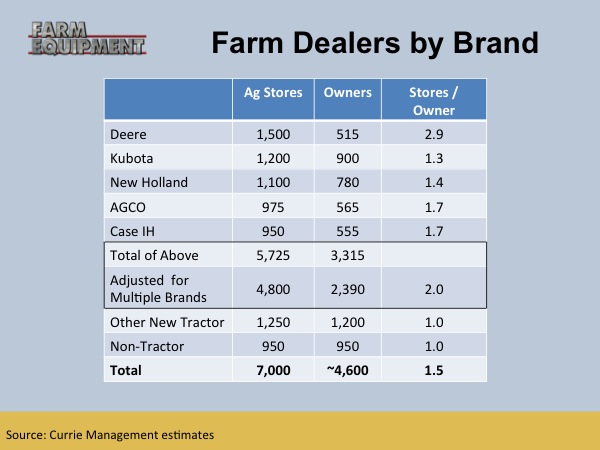

It’s actually challenging to determine the number of North American dealers each of the major manufacturers have for a variety of reasons. By Russell’s estimates, ranking them by the number of ag stores that they have, Deere is at the top with 1,500 locations, 515 owners with an average of 2.9 stores per owner. Kubota is next with 1,200 stores, 900 owners and an average of 1.3 stores per owner group. They’re followed by New Holland with 1,100 stores, 780 owners and 1.4 stores per owner. Next is AGCO with 975 locations, 555 owners and an average of 1.7 stores per owner. Last on the list in terms of total number of dealer locations is Case IH with 950 stores with 555 owners averaging 1.7 stores per owner group.

Obviously there’s some overlap. Taking out the cross-branded dealerships it comes out to 4,800 locations and 2,400 owners, or an average of about two stores per owner.

When the “non major brands,” for example, those carrying Versatile tractors, those that don’t sell tractors and sell non-powered equipment or sprayer dealerships, are included the total is 7,000 stores with about 4,600 owners averaging 1.5 stores per owner.

Dealers by Size

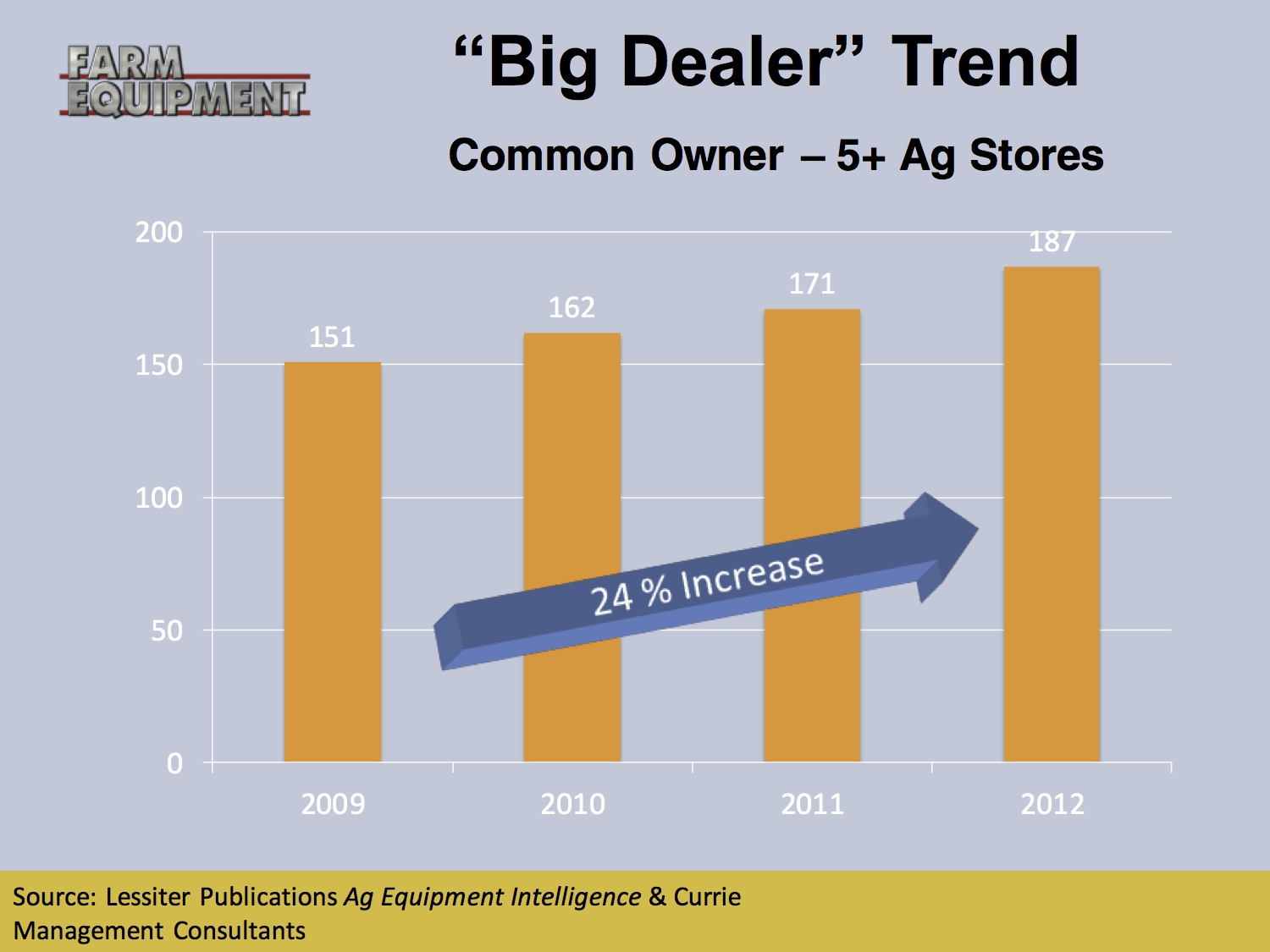

Russell explains that when he classifies farm equipment dealerships as “Big Dealers,” this indicates each dealer or dealer group operates at least five store locations. “We work with Ag Equipment Intelligence each year to track consolidation trends among ag machinery dealers and the data is included in the “Big Dealer” report issued each April.

“One thing is certain when we look at these trends is that consolidation is happening very fast,” says Russell. In the industry, about one in every four dealers is part of a dealer group that has five or more ag locations: for Deere it’s about 60%; Case IH about 40%; AGCO one in every four; New Holland 14%; and for Kubota about 8% of their total locations are owned by dealers that operate five or more stores.

“Deere clearly went out early on the consolidation pushed and the other brands are doing that as well at different rates,” says Russell.

Looking at the overall industry, the trend is clear. Since Ag Equipment Intelligence and Currie Management Consultants began tracking consolidation trends in 2009, there’s been a 24% increase in the number of “Big Dealers” operating farm equipment locations in North America.

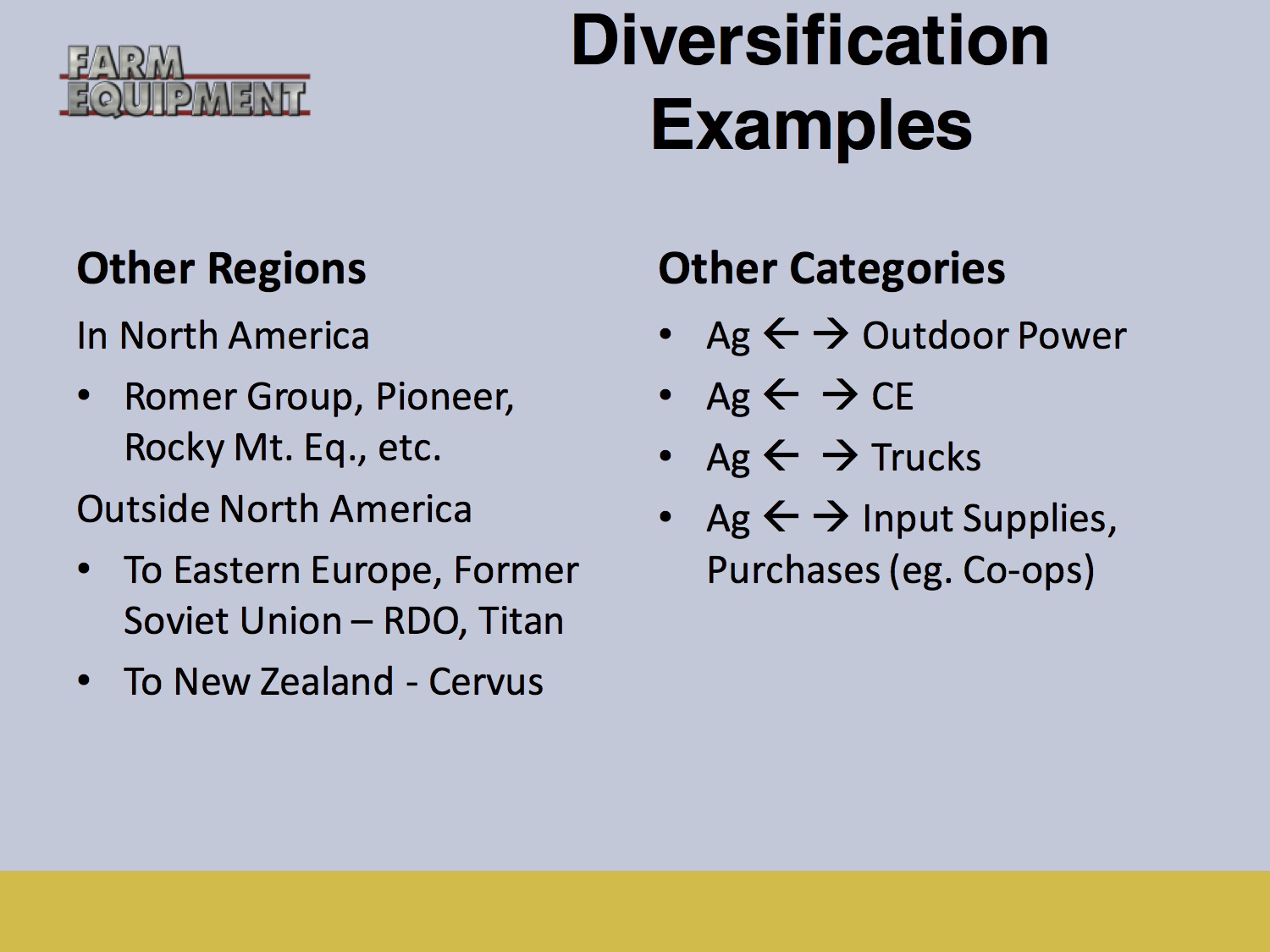

Globalization & Diversification

It’s no secret that the world is getting smaller for the farm equipment industry as both dealers and manufacturers move across the globe to expand their businesses. This desire to expand, regardless of the region, is another major driver that is reshaping how farm equipment dealers view their business and diversifying in the path to growth.

While manufacturers have been spreading their wings worldwide for decades, more recently dealer groups have been making their way overseas.

As far as dealers going global, Russell points to John Deere dealer group, RDO Equipment, that is doing business in Russia and Australia. In the past few years, Cervus Equipment, another Deere dealer, has established itself in Australia and New Zealand. The biggest of all Case IH dealer groups, Titan Machinery, is up and running in Romania, Bulgaria and Serbia.

Closer to home, Russell says, in the past most dealers chose to expand into areas that were contiguous to existing location, but that model is no longer set in stone. Examples of dealers expanding into various regions include Pioneer with locations in California, Texas and Idaho. The Romer Group, which has locations in Colorado and Wyoming, also owns James River Equipment with stores in Virginia, North and South Carolina.

Rocky Mountain Equipment has operations in Alberta and Manitoba and Saskatchewan where there is significant distance between locations. “What is happening is dealers have found they can operate effectively a long way from home and do not need to be contiguous,” says Russell.

They’re also diversifying their business and moving more heavily into construction equipment, compact construction machinery, outdoor power equipment, over-the-road trucks and in some case industrial machinery, like fork lift trucks.

According to Russell, the industry is also seeing increased globalization in the manufacturing sector of the industry. Thanks to globalization, North American manufacturers are competing with companies all over the globe, and vice versa.

Besides the major manufacturers building manufacturing facilities and setting up sales organizations all over the world — from Brazil to Africa, and Russia to China — full-line and shortline equipment makers are also expanding their overseas efforts.

Russell discussed a number of manufacturers that are adding lines with the goal of becoming full-line manufacturers, like Kubota, Claas and Rostelmash/Buhler. And they’re all looking for dealers.

“The point is there are more and more manufacturers that are adding lines and coming to you or your competitors and saying, ‘Distribute our product for us,’” says Russell. “If you’re an effective dealer and know how to sell equipment and support a sustainable business, you’ve got people knocking at your door, coming after you.”

The lesson to learn from the rapid implementation of technology is it allows dealers and their customers to be more connected, says Russell. “Technology allows you to be closer to the customer.”

He gives this example: a farmer with a cell phone means he can pick up the phone and talk to the dealership’s service manager very easily. “With farming, we used to be vulnerable to distance. It took a long time to drive out to the farm at the other end of the county, talk about a sale and then come back two or three times,” Russell says. “If the guy broke down, how do you get the parts out to him or how does he bring the machine into the shop? Distances were a problem. Now with cell phones and remote telemetry, you’re in a situation that you’re able to connect and actually know what’s happening with the farmer’s machine before it fails. This is state of the art.”

“Dealers that are more successful have to collaborate with the other suppliers in the business.”

Taking full advantage of technology means dealers should also be employing customer relation’s management, which will helps them know every customer in their area, their characteristics, what they buy and how to contact them. Technology is making it increasingly easier for customers and dealers to communicate with each other.

“Take advantage of it, leverage the technology so no longer do we have to be victim to those distances that have been a problem in farming,” says Russell. “We now can take advantage of that and learn how to run our businesses differently by using that technology to our benefit.”

Russell puts it simply: technology is a multiplier.

“Farming has always been that. From the time Cyrus McCormick invented the reaper and one man could do the work of 40, that’s what our business is. It’s about replacing people with capital. That’s what needs to happen in your dealership as well — using technology to replace people with capital and processes,” he says.

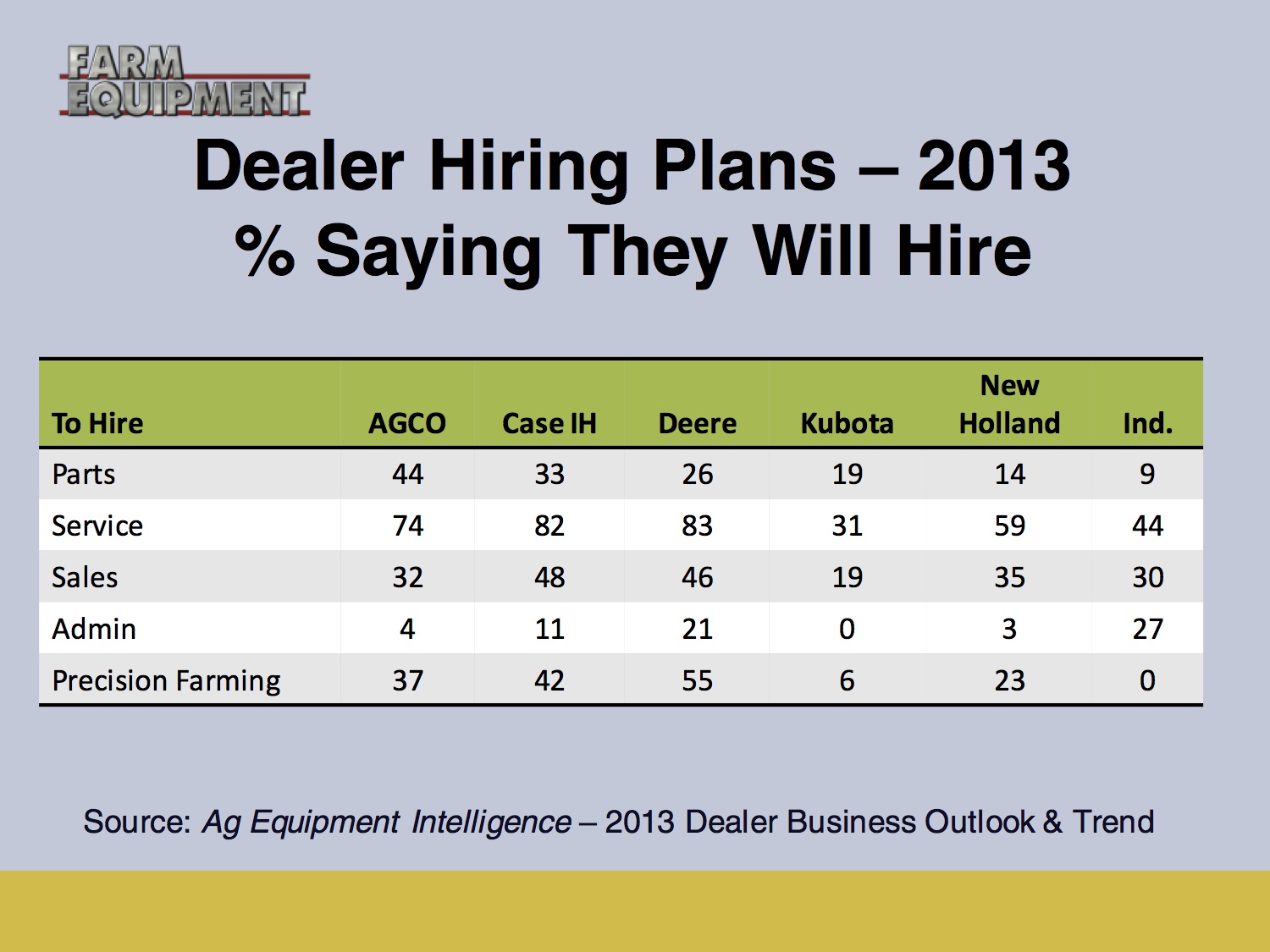

He also points to how dealer hiring plans have also shifted in recent years with the introduction of precision farming practices and equipment.

“Everybody wants technicians, but more and more dealers need precision farming specialists. As this demand grows, the questions for dealers become, where are you going to get these specialists? How are you going to train them?”

The People Factor

Finding and training technicians and precision farming specialists rank high on dealers’ list of biggest concerns. “There’s a demand for these people. Where are you going to get them? How are you going to train them? These are some of our most significant challenges,” says Russell.

“What are the lessons we take away from this? Your customers are changing, they’re consolidating, they’re more sophisticated, and they’re more connected. How do you find and hire the employees and train them to serve these more sophisticated and demanding buyers? That’s is one of the major drivers in the push for consolidation — leveraging people. Your people must be more adaptable to the changes that are happening in our industry, starting with the end user,” emphasizes Russell.

“From the time Cyrus McCormick invented the reaper and one man could do the work of 40, that’s what our business is. It’s about replacing people with capital.”

A service manager who is very good technically now needs to be able to diagnose and troubleshoot precision farming equipment. He also needs to manage the productivity of the other technicians and keep on top of paperwork to keep work in process running smoothly. He may even have to juggle multiple locations, and that means adaptability is a must, Russell says.

“He needs to be able to do a lot of different things in your dealership. This is just one example of hiring employees who are adaptable,” he says.

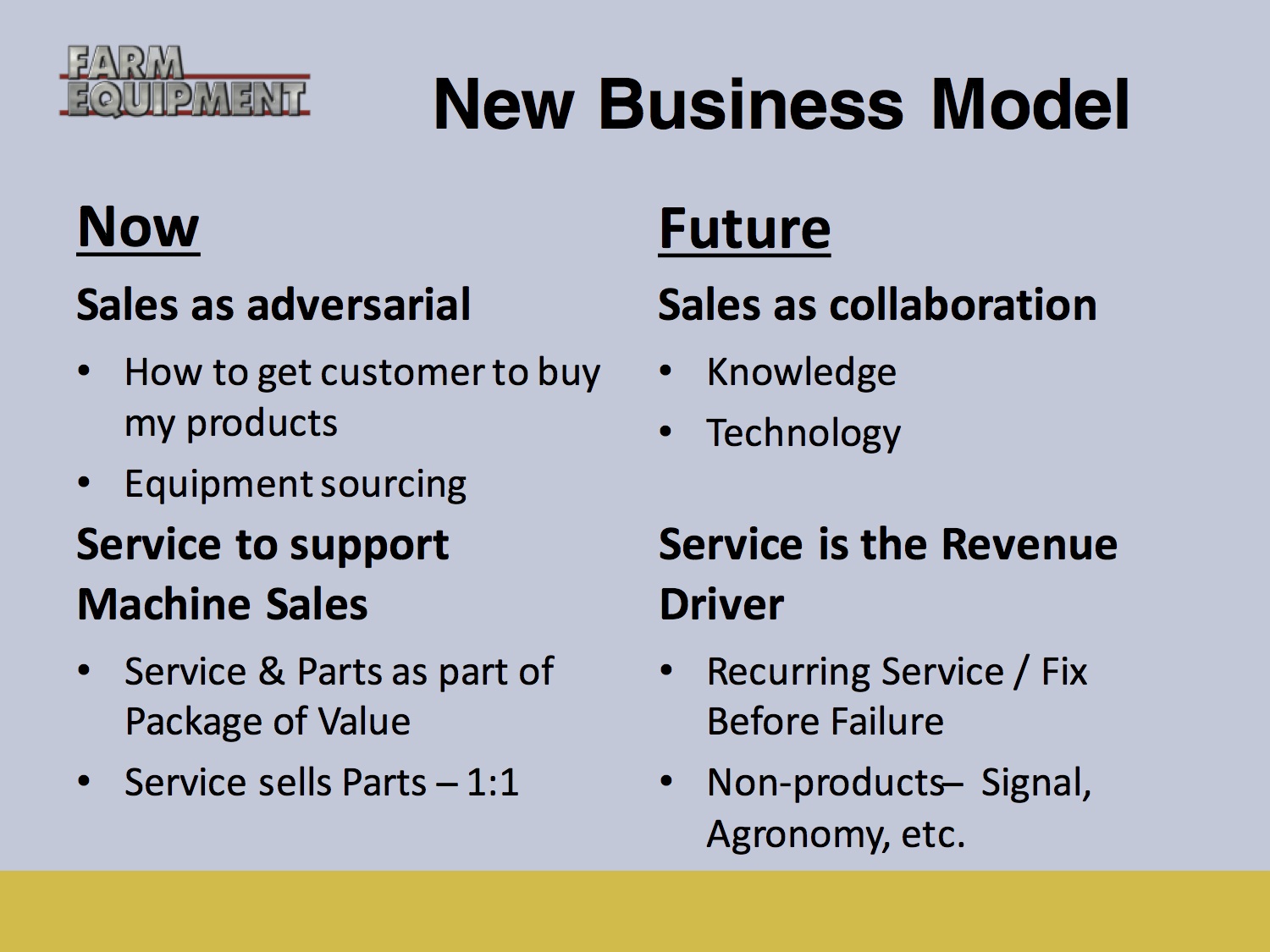

A New Business Model

Evolving technology is forcing the industry to change how it makes money in this business. Russell says we’re moving from selling tangible products and services to intangible services.

“Traditionally, the dealership’s service department worked on a piece of equipment and sold the capability of the technicians as well as the parts that are on that equipment,” Russell says. “But now you’re selling a signal for RTK, or agronomic advice or you’re talking about how to troubleshoot or make that yield monitor work. These are more intangible; it’s not like a piece of iron like a tractor or a part.”

Making that transition from pushing iron to selling service is critical for success, Russell suggests. “Some iron people can’t make that transition from selling iron to selling services. And what this means is that dealers who are most successful will need to collaborate with the other suppliers in the business.”

Russell describes the current business model for sales as adversarial — trying to sell at a high price while the customer is trying to buy at a low price. At the same time, service is viewed as a way to make money and capture new customers resulting in selling more service and more parts. “That’s the way it is now. That’s how successful dealerships operate,” he says.

However, in the future that model will move from adversarial to collaborative.

“You’re now selling knowledge, just like that service manager is trying to diagnose things over the phone. The question is how do you monetize that; how do you make sure that when he’s on the phone selling his expertise or giving advice, that you’re getting paid for that? In other words, how do get paid for providing solutions,” says Russell.

“So now we’re moving to selling services on the service side itself; you’re trying to convince that A-level customer that he should have a long term maintenance contract with you; why he should bring his machines in regularly for inspection programs during the winter so you have fixed it before failure. Ultimately, you’re selling other value as well.”

“The pace of change in the business is happening very fast. It’s difficult to hire and keep good people, but that’s the critical issue in your business.”

Russell likens the business model of the future to three axes. On the Y-axis or vertical axis is a plant the farming is growing. With that is the seed, fertilizer and chemicals that the agronomic people need to worry about. The dealer’s responsibility and expertise is the X and Z-axes. “You’re dealing with area. You have that technology with a yield monitor and the auto-steer and all the other things that allow the farmer to operate over a wide area,” Russell says. “The data starts with the machines that you sell and support. So embrace that, number one, but also learn how to work collaboratively with the other people, including the agronomic suppliers.”

Russell says that over the years Currie Management has found two key things when it comes to an effective business model. First, the fastest way to grow the top line revenue is with customer relation’s management — an active system to know every customer in your area combined with the discipline of your sales people to make sure they know exactly who they’re calling on. And then, of course, calling on the right people and the right frequency.

Number two is performing aggressively and managing expenses to specified targets. “Know what the targets are and how to meet them. More and more, expanding dealers tend to specialize more because they can manage their costs better. So this comes back to the question about focus vs. diversity,” Russell says.

Back to the Basics

The ultimate business driver for every dealership comes down to the very basic question for any business: how can it make money. “We are moving from profitably selling tangible services and parts to profitably selling service intangibles. Today, dealers are selling a signal for RTK or advice and expertise about agronomic issues. It’s not a piece of iron like a tractor or a part. This is a major change for most dealers.”

Another business basic business that hasn’t changed is what the best performing dealers truly focus on. And that’s expense control. “For these larger operations, the top line isn’t what’s important, it’s the bottom line, and the only way to get the bottom line is to worry about and pay attention to your expense control,” says Russell.

Ultimately, he adds, it’s about talented people.

“What we’ve found in analyzing the most successful consolidating dealers is that there are very few economies of scale. Well-run dealers are well run, Russell explains. “Most of a dealership’s costs are the cost of goods sold from the manufacturer. That’s not going to change. If you’re a $100 million or $200 million business, you still need to buy that piece of equipment or those parts. Yes, you’ll get some volume discount, but most of your cost in this cost of sales or it’s about your people. But how you run that operation with the people and how you leverage them is the key thing in a consolidating organization.”

George Russell’s Key Points

Growing Expectations: The expectations of quality for your customers ad prospects are increasing faster than the average non-farm family.

Get Connected: Technology allows for rural populations to be closer, networked, precise and vocal — so you must too.

Technology: Technology is a multiplier — farm machinery has always done that and will do so even more with electronics, communication and software.

Concentrated Agriculture: Concentration of dealers is driven by the concentration of agriculture as well as increased value added of large area and leverage of processes and people. The concentration of agriculture will continue until farm globally can feed 9 billion people.

People Factor: It’s all about (talented) people — economies of scale for a well-run operation are not as large as most people think. Finding and training people may be your biggest challenge in the future — technicians as well as other key roles. Learn to coach and how to train other coaches.

Organic Growth: The fastest way for top line organic growth is active customer relations management, and a disciplined approach to sales management.

Service Matters: Service sells, service pays.

Expense Management: The best financially performing dealers manage expenses to targets and achieve this only by aggressive expense recovery.

Focused Diversification: Diversification is a good portfolio investment strategy, but maintain your focus vis a vis the number and hidden expenses of shortlines and emerging opportunities.

Distribution Needs: More and more farm equipment companies need distribution.

Service Star: Put your best available manager in service — most challenging and one with most leverage on performance. Also flexible enough that he could jump into another role like sales, parts, etc.