The row-crop tractor market is beginning to show signs of life again. After several years of volatility, the data is pointing toward a more stable environment — one where supply has adjusted, values are strengthening and transaction activity is returning.

What we are seeing, however, is not a return to the strength of prior years — it is a market stabilizing on top of underlying financial pressure, and the results of trade cycles from a different commodity outlook. Over the past several years, row crop profitability has shifted from roughly $1.50 per bushel in 2021 and 2022 to losses of around $0.50 per bushel more recently. That swing hasn’t broken the system — but we’ve all felt the drain.

What does stabilization look like? Across key segments, inventory levels have tightened. Dealer supply for 175-99 horsepower tractors is down approximately 24% year-over-year, while larger 300-424 horsepower units are down closer to 14%. At the same time, unit turns have stabilized. Not necessarily because demand has surged, but because inventory has come back in line.

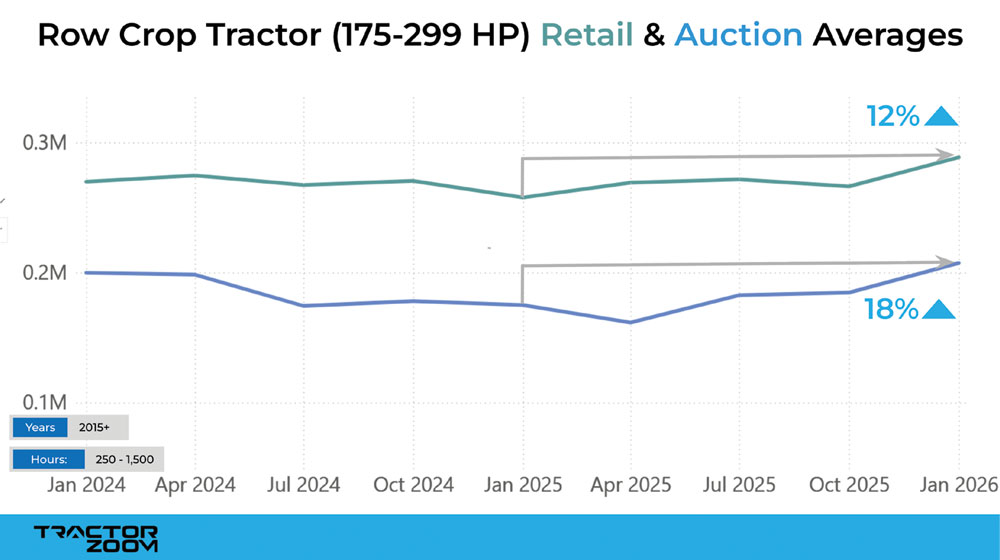

Auction values are responding accordingly to this tighter supply. At the block, lower-hour machines in the 250-1,500-hour range have rebounded meaningfully. Over the last year they were up roughly 18% for 175-299 horsepower tractors, as seen in Fig. 1, and 13% for the higher horsepower units compared to a year ago. Even higher-hour machines saw modest improvement, with values up about 4% of the last quarter in 2025.

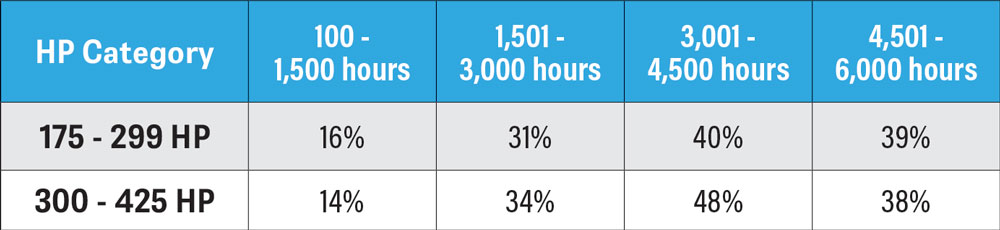

Table 1, % of Row-Crop Tractor Inventory Sold in 60 Days. Tractor Zoom Pro

Retail list values of this used tractor category are showing increases of similar magnitude —12% year-over-year on average as seen in Fig.1. For a specific example, late-model John Deere 8R 280 tractors that are less than 3 years old with 500-1,500 hours have seen asking prices increase approximately 9% year-over-year, with actual sold transaction values climbing even more.

On the surface, that may look like a recovery. In reality, that increase in low hour tractor values may be more “signal distortion” than “surging demand.”

A Recovery That Isn’t Even

Part of that distortion in today’s market is the divergence between and within equipment segments.

Late-model, lower-hour machines are seeing higher retail prices, and have been a bright spot for some dealers in an otherwise bleak 2025. For others, those high list values are a result of higher used trade premiums and now, along with a shifting farm profitability outlook, are causing those low hour, and high-priced machines to stick around for longer than normal. Table 1 below shows the current percent of U.S. dealership’s row-crop tractor inventory that moves off the lot within 60 days. The fastest moving category is the 3,001 – 4,500 hour segment for both the 175-299 and 300-425 horsepower tractors.

Fig. 1, average row-crop tractor value trends at retail and auction. Tractor Zoom Pro

Higher-hour equipment tells a different story. The recovery has been slower and less consistent. That suggests that third and fourth-cycle used buyers — those typically purchasing older equipment — are facing more financial pressure.

We are seeing lower hour machines take longer to sell, especially within the higher horsepower range.

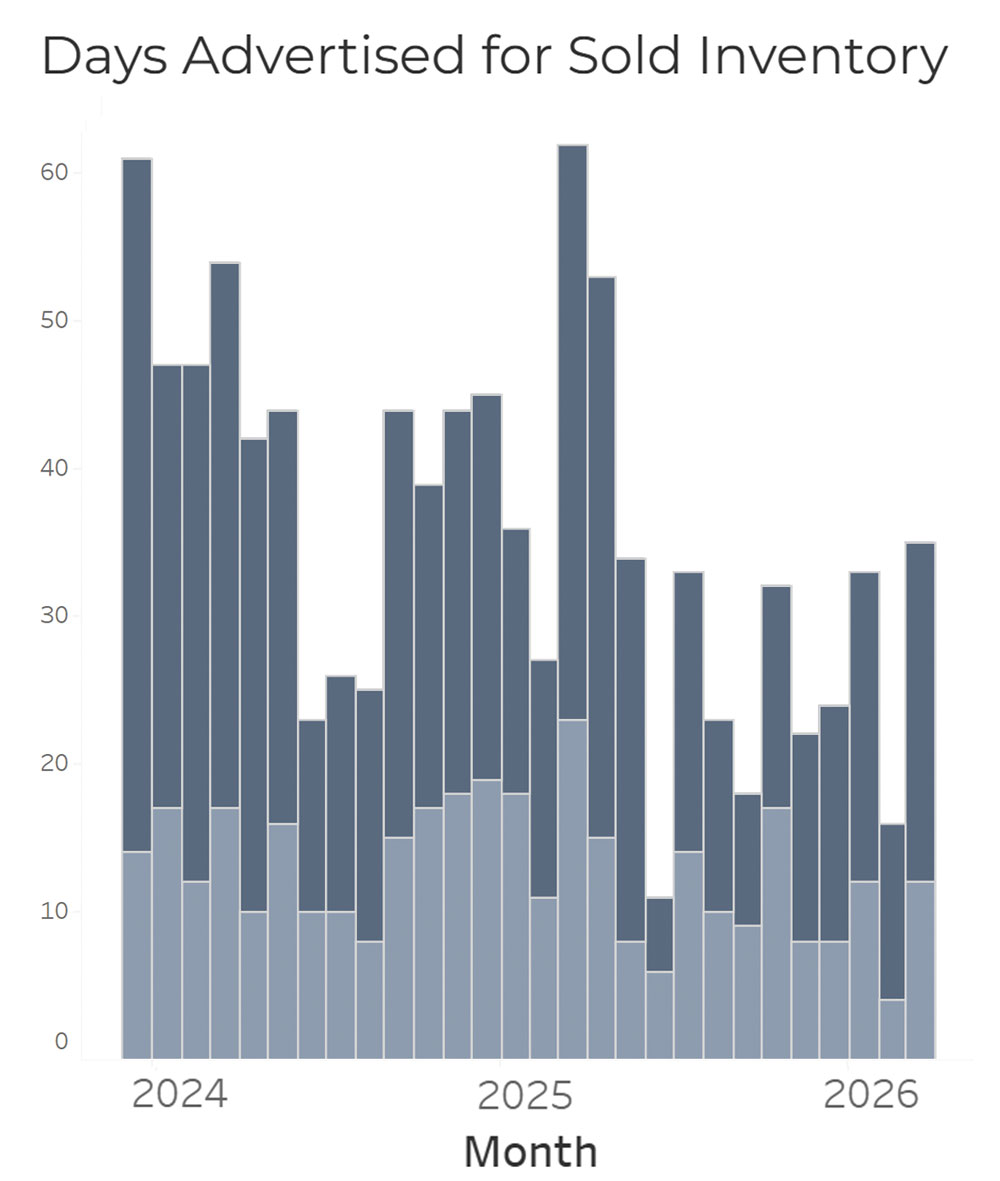

Fig. 2, tractors between 100-1,500 hours sold in less than 60 days. Tractor Zoom Pro

Then, concentrating on just the higher horsepower category of low hours 100 – 1,500, we’ve seen this trend downward from 2024 where 37% sold in the first 60 days, to 23% in 2025, to now just 14. Fig. 1 shows, month by month, that decreasing amount sold in less than 60 days.

Contrast that with the same horsepower category of tractors between 3,001 – 4,500 found in Fig. 3. This grouping has had rising sales and its highest amount sold in 60 days since May of 2025.

Fig. 3, tractors between 3,000-4,500 hours sold in less than 60 days. Tractor Zoom Pro

Either way, this is not a return to the kind of demand environment we experienced in 2021 and 2022. It is more tempered and more selective. And that changes how our dealerships need to operate.

What Dealers Do With This Information

The takeaway is not just how the market is behaving — it’s how to respond to it with more discipline.

In an environment this dynamic, dealerships need tighter visibility into their own sales analytics. That starts with tracking key indicators like time-to-sale, percent of inventory sold within 60 and 90 days, risk ratings and price position relative to market. These metrics provide early signals of whether inventory is aligned with real demand — or drifting away from it.

Just as important is tracking used trade premiums. When trades are taken at values that assume stronger future demand, but that demand does not materialize, inventory lingers and margin erodes. Monitoring trade premiums against actual sales velocity helps ensure inventory levels — and cost basis — stay in line with what the market will support.

From there, execution becomes the lever. Sales process fundamentals — early buyer identification, consistent follow-up and disciplined pricing adjustments — are what convert inventory into cashflow. Speed matters. The longer a unit sits, the more likely it is to require a pricing concession.

This market is offering opportunity, but only for those measuring it closely and executing against it with consistency.

Trade Values & Trends is brought to you by Tractor Zoom.

Tractor Zoom transforms and connects big data into real-time actionable insights, accelerating a dealership’s heavy machinery and farm equipment business. Our solution, the only one providing transparent, comparable sales data, connects multiple data systems into one easy to use CRM and equipment valuation platform, empowering dealers to optimize decisions, maximize inventory turns, and increase your team’s efficiency and effectiveness. Spend less time on unproductive tasks and more time growing your customer base as we revolutionize the way you drive profitable decisions in the equipment industry.

Andy Campbell is the Director of Insights at Tractor Zoom, where he helps equipment dealerships turn data into faster decisions, better alignment, and stronger margins. Raised on a multi-generation Iowa farm, Andy blends deep ag roots with experience in Fortune 500 companies, tech startups, academia, and as a consultant to make sense of what’s really driving the farm equipment market.