In late December 2017, President Donald Trump signed the Tax Cuts & Jobs Act into law, marking the first significant tax reform in the U.S. since the Reagan administration in the 1980s.

“It moved through Congress very quickly. The bill was introduced on Nov. 2, and the president signed it by Dec. 22. And in terms of Congress, which normally moves at a glacial pace, this was lightening fast. And so that really precipitated our efforts to quickly get an amendment, which were very limited in this legislation,” says Eric Wareham, vice president of government affairs for the Western Equipment Dealers Assn. (WEDA).

One important amendment for farm equipment dealers is the floorplan interest amendment, which WEDA and the Equipment Dealers Assn. worked with Congress to include in the bill.

C Corp vs. S Corp

One change to the tax code that is good news for dealers is the corporate tax rate was permanently reduced to 21% starting in 2018. Curt Kleoppel, president of Equipment Dealer Consulting and CFO of WEDA, says this is particularly good news for dealerships that operate as C Corps. It represents a pretty significant tax break, he says, noting that previously dealerships could have been in 39% rate. Additionally, it will take legislative action to change the rate again.

At a Glance: Business Tax Rates & Provisions

Corporate Rate permanently reduced to 21% beginning in 2018.

Pass-Through Business Income establishes a 20% deduction of qualified business income from certain pass-through businesses. Specific service industries, such as health, law and professional services, are excluded.

Alternative Minimum Tax for corporations is eliminated.

Full Expensing allows full and immediate expensing of short-lived capital investments for 5 years.

Sec. 179 Expensing limits are increased to $1 million per year with phase-out beginning at $2.5 million. Indexed for inflation after 2018.

Cost Recovery (Bonus Depreciation) is allowed for used property, and is permitted at the 100% rate through 2022, and phased down by 20% each year thereafter.

Net Operating Loss eliminates net operating loss carrybacks and limits carryforwards to 80% of taxable income. Farming businesses still allowed a 2-year NOL carryback.

Agricultural Cooperatives receive a 20% deduction on pass-through income that will be calculated on the gross income of the cooperative beginning in 2018 in lieu of the domestic production activities deduction (Sec. 199), which is repealed.

Cash Accounting is maintained for farming businesses.

LIFO accounting method is maintained.

Repatriation enacts deemed repatriation of currently deferred foreign profits at a rate of 15.5% for cash and cash-equivalent profits and 8% for reinvested foreign earnings.

Territorial System eliminates worldwide system and moves to a territorial system with base erosion rules.

With such a large tax cut for C Corps, businesses that are S Corps may wonder if now’s the time to switch structures. Kleoppel urges dealers to discuss the options with their tax advisors or CPA. “You have to run through the numbers. There are so many things involved, especially with some other provisions. Each situation is going to be unique,” he says.

“In some cases it would probably be wise to switch from S Corp to C Corp. For others, it’s probably best to stay a S Corp because the individual tax rates have lowered, and they’re good until 2025. Granted at 21%, the corporate rate is now a lot lower than most individual income tax rates, but again with everything else that’s going on in this tax reform bill, you’ve got to do some number crunching before you make that decision. Like I said, it’s great for C Corps now, and it’s another reason to stay a C corp. But whether or not you want to change from S Corp to C Corp, I’d recommend you run through the numbers and see exactly what the tax savings would be.”

One change that is beneficial for S Corps are the breaks for pass-through business income. For partnerships, sole proprietorships and S Corps, the law established a 20% deduction on qualified business income, explains Wareham. However, Kleoppel warns it is fairly complicated. “It’s not just, ‘OK, I got a K-1 worth $700,000 of income, and I get a $140,000 deduction on my tax return. I pay tax on $560,000.’ It’s not quite that easy. And what they’ve put in as a condition is a couple things and one is taxable income. So if you’re a single person and have taxable income of $157,000 or more, or if you’re married filing jointly and have taxable income of $315,000 or more, there could be limitations,” he says.

At a Glance: Floorplan Interest Amendment

Small Business Exemption fully maintained for businesses with less than $25 million in revenue. Farming businesses with income greater than $25 million can retain interest deductibility if they use the Alternate Depreciation System for investments.

Limitation on Deductibility with Floorplan Interest Amendment deduction limited to the sum of (1) business interest income; (2) 30% of the taxpayer’s adjusted taxable income for the tax year; and (3) the taxpayer’s floorplan financing interest for the tax year. Any disallowed business interest deduction carried forward indefinitely (with certain restrictions for partnerships).

Definition of Floorplan Financing Interest: Interest paid or accrued on indebtedness used to finance the acquisition of farm equipment held for sale or lease to retail customers and secured by the inventory so acquired. Does not include construction machinery and equipment.

Trade-Off for Using Floorplan Interest: Full expensing disallowed if floorplan interest factored into deduction. Sec. 179 expensing still maintained if floorplan interest used.

There are of course limitations and Kleoppel offers this example to highlight them. Sticking with $700,000 of K-1 income from the previous example, a 20% deduction would be $140,000. But, one of the conditions is a business has to claim whatever is lower between the 20% of qualified business income or 50% of the total wages paid by the business. “Say it’s a one person sub S, and you have that $700,000 dollars of K-1 income, and you don’t take any wages out. Well guess what? You don’t get a deduction because the lesser is the 50% of wages paid, which is zero. So in this case, you don’t get a big benefit out of it,” he says.

However, Kleoppel points out most S Corp dealerships have a large amount of wages being paid out to employees, so most of the time dealers would get the 20% deduction on qualified business income. “If you had $500,000 worth of wages paid, and 50% of that’s $250,000. Well the lesser is the 20% of the $700,000, which is $140,000. So you would get a nice deduction.

“And that’s why I come back to needing to think about it before switching to a C Corp. If you look to see if that 20% deduction actually applies, and you apply it to the current tax rate at the individual level, and throw in your standard deduction of $24,000, a 35% tax rate could actually go down to where the effective tax rate is 5-7% lower because you’re eliminating $140,000 of income hopefully. Your effective tax rate could go down to 20% depending on the circumstances. That’s why I say you have to do some number crunching.”

Expensing Provisions

There were some changes in the expensing provisions, including full expensing and Sec. 179 expensing. Wareham says full expensing allows for full and immediate expensing of short-lived capital investments purchased for the next 5 years. After 5 years, this provision will be phased out. Kleoppel adds that the full expensing provision applies to both new and used equipment.

After years of wondering what Congress was going to do about Sec. 179 each year, the Tax Cuts & Jobs Act made Sec. 179 expensing permanent and increased the limits to $1 million per year with phase-outs beginning at $2.5 million.

“As your dealerships know, a couple of years ago, we waited in the middle of December before it was determined whether or not it was going to be a $25,000 limit or a $500,000 or $750,000 limit. We finally heard from Congress what the dollar amount was, and I think it was about Dec. 15. Well, that put a lot of producers and dealerships at odds. You try to get things done within a 2-week period, and of course one of the provisions for Sec. 179 is that the asset actually has to be put into service,” Kleoppel says. “It’s good that it’s permanent, and you can do a lot of good tax planning now whether you’re a producer or own a dealership, it’s a lot better for you.”

“A lot of the tax breaks that are favorable for dealers are also favorable for farmers and will give them some cushion …” — Eric Wareham, Western Equipment Dealers Assn.

Another bit of good news is that Bonus Depreciation is permitted at the 100% rate through 2022, and it will then be phased out by 20% each year. “This is another one of the good parts of the provisions, and it helps offset if you can’t qualify for full expensing. Between Sec. 179 and bonus depreciation, you’re really not hurt that much by not having full expensing,” says Kleoppel.

Floorplan Interest Amendment

The aspect of the act that carries the most weight for farm equipment dealers — and wasn’t part of the original bill — is the floorplan interest amendment.

“The interest deductibility portion of the original House Ways and Means bill only provided an exemption for businesses with less than $25 million in revenue,” Wareham says. “And we said, ‘Hold on a sec. This does not work for equipment dealers.’ We knew all along that behind the scenes, the discussions were centered around full expensing, and everyone was excited about the full immediate expensing. And that is going to be great for our economy, but there has to be a trade off for the fiscal scoring. And all along the trade off was intended to be removing the business interest deduction.”

WEDA, EDA and others worked with the House Ways and Means committee on the floorplan interest amendment. Here’s how Wareham describes it. “Limitation on deductibility with floorplan interest, the deduction is limited to the sum of your business interest income, 30% of your adjusted taxable income, and your floorplan financing interest for the tax year. It is important to note that any disallowed business interest deduction will be carried forward indefinitely. We don’t really need to worry about that because the way this is written, it ensures that we can always write off 100% of that floorplan financing interest,” he says.

For the sake of this amendment, Wareham says floorplan financing interest is defined as “interest paid or accrued on indebtedness used to finance the acquisition of farm equipment held for sale or lease to retail customers, and secured by the inventory so acquired.”

The floorplan interest amendment is electable from year to year, Wareham says. It’s important to note that this provision does not include construction machinery and equipment. Wareham and Kleoppel say that for equipment that has dual use — such as skid steers — and are financed by an ag OEM and you have an ag contract with the company, then it would come under the floorplan interest. However, if the dealership is a straight construction dealership and has no ag contracts, it would not apply to floorplan interest.

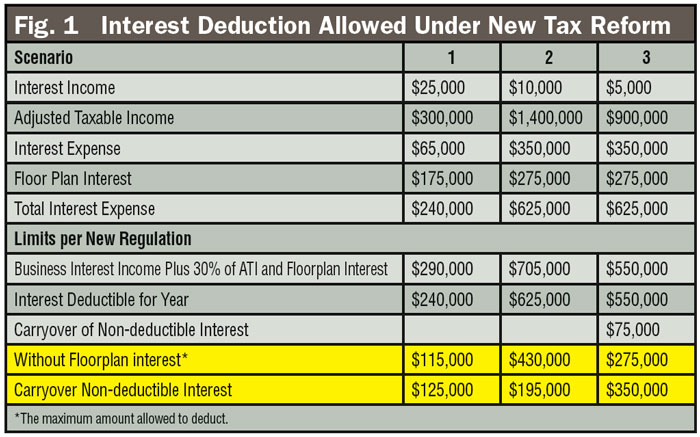

Figure 1 highlights three scenarios of the interest deduction allowed under the new reform. In scenario 1 the dealer has $25,000 worth of interest income. His adjusted taxable income, which is basically taxable income before interest depreciation, etc., is $300,000.

The dealership has $65,000 of regular operating interest expense. That could be a regular bank credit line used for operating, if a dealer is trying to buy out a shareholder, or if the dealership had an expansion and had to borrow some money. This is not connected to inventory. And then he has floorplan interest of $175,000. The dealer’s total interest expense is $240,000.

To figure out the amount that would be allowable, Kleoppel says you take the business and interest income, plus 30% of the adjusted taxable income and the floorplan interest. “You would be allowed $290,000 maximum deduction. You only have $240,000, so you’d be allowed your total interest deduction,” he says.

Farm Equipment hosted a webinar in early January reviewing the major changes that came with tax reform. To view the webinar and for additional details on the 2017 Tax Cut and Jobs Act, including information on personal tax rates and provisions, visit www.Farm-Equipment.com/0218.

Scenario 2 shows a situation with larger income numbers and a little more interest. In this example, the dealer has $10,000 of interest income, $1.4 million of taxable income and $350,000 of interest expense, which, Kleoppel says is pretty heavy. “But if a dealership that has gone through expansion, or bought out a major shareholder, it can get up to $350,000 of interest expense pretty quickly,” he says.

This dealer also has $275,000 in floorplan interest, so his total interest expense is $625,000. Under the guidelines, he’d be allowed $705,000. In this scenario, the dealer would be able to deduct all of his interest expense of $625,000.

In scenario 3, the dealer’s interest income is $5,000, the taxable income is a little lower, and the interest expense stays the same at $625,000. “When you go through the calculation, and you’re allowed the maximum interest deduction of $550,000. Of that, you would be carrying over $75,000. So you’d be disallowed $75,000 of that operating expense deduction,” Kleoppel explains. “And there’s also an impact if you had a loss, or zero taxable income, if you had regular interest expense that was not floorplan interest.”

The highlighted area in Figure 1 shows what can happen in all three cases, without the floorplan interest amendment. In scenario 1, the dealer would only be allowed $115,000 and would have a carryover of $125,000 of interest. In the second scenario, he’d only be allowed $430,000 without this amendment exclusion, and then the carryover would be $195,000.

At a Glance: Personal Tax Rates & Provisions

Standard Deduction doubled to $12,000 for individuals or $24,000 for married couples.

Itemizing

- SALT (State and Local Tax) Deduction Limits the state and local tax deduction to a combined $10,000 for income, sales and property taxes;

- Home Mortgage Interests Deduction is maintained for one home up to $750,000

Charitable Deduction is maintained.

Capital Gains rates are largely left unchanged.

Sec. 1031 Like-Kind Exchanges are maintained for real property transactions.

Retirement Savings Provisions around 401(k)s and IRAs are maintained.

Health Insurance

- Individual Mandate is repealed beginning Jan. 1, 2019;

- Medical Expense Deduction is maintained for expenses exceeding 7.5% of AGI in 2018 and 10% beginning in 2019;

- Health Savings Accounts tax treatment is maintained.

Child Tax Credit is expanded to $2,000 per child (phase-out begins at $400,000 income)

Alternative Minimum Tax is retained on personal filings, but raises the exemption on the alternative minimum tax from $86,200 to $109,400 for married filers, and increases the phase-out threshold to $1 million.

Estate Tax Relief is granted by doubling the exemption amounts ($11 million for individuals; $22 million for couples) through 2025; reverting to current amounts thereafter.

Stepped-up Basis is maintained.

“In the third case — just by chance with the numbers that I picked — he would be allowed $275,000, which is his floorplan interest oddly enough. But the carryover would be $350,000. So again, without this amendment, we could have been impacted pretty heavily. So I think for the most part, we’ve saved a big deduction for the dealership, so I think it’s a pretty big win,” Kleoppel says.

Kleoppel adds, “The big amendment to this deal is with the floorplan interest exclusion. Whether you have zero income or not, you’re going to get that 100% deduction for your floorplan interest, which is big because that’s the biggest part of the interest on most dealership’s income statements.”

Wareham says there is one trade off for using the floorplan interest deduction, and that is full expensing is disallowed for farm equipment dealers when the floorplan interest deduction is used. “We ran a lot of numbers to make sure that Section 179 expensing is maintained if floorplan interest is used, and also the bonus depreciation. We felt that would cover the vast majority, if not all of the dealers in the event that they can’t use full expensing,” he explains.

Post a comment

Report Abusive Comment